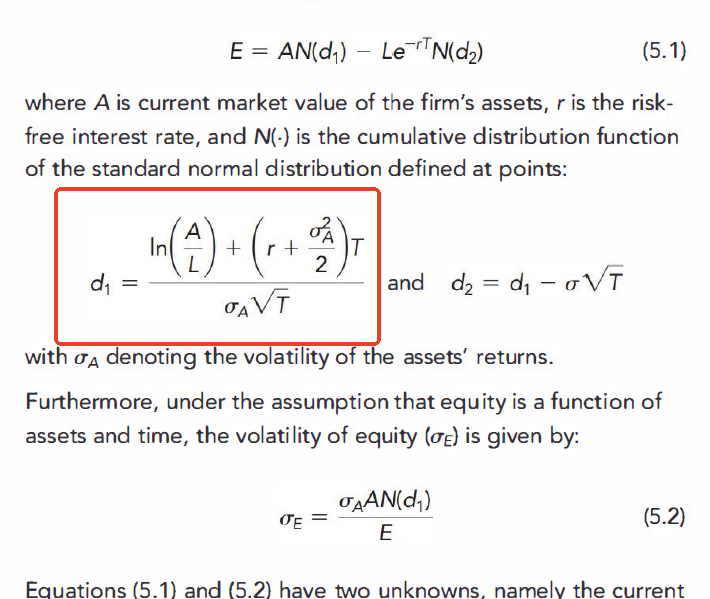

NO.PZ2024042601000015

问题如下:

A portfolio manager at a hedge fund is applying the Merton model to estimate the volatility of a non-dividend paying firm whose equity shares are held in the fund’s portfolio. The manager conducts preliminary analysis on the firm and obtains the following results:

- Value of equity: USD 45 million

- Value of the firm’s only debt maturing in 5 years: USD 60 million

- d1: 3.217790

- d2: 3.038905

选项:

A.6%

8%

C.16%

D.18%

解释:

本题中d1的公式似乎与教材上的有些不同?教材上的d1公式分子里有一个r,而这题答案解析里没有,这是以哪个为准呢