NO.PZ2019010402000019

问题如下:

The market price of the put option is overpriced relative to the binomial option pricing mode, what the positions the manager could have to take arbitrage opportunity’s advantage?

选项:

A.

short put and buy the underlying

B.

long put and buy the underlying

C.

short put and short sell the underlying

解释:

C is correct.

考点:No-arbitrage approach

解析:

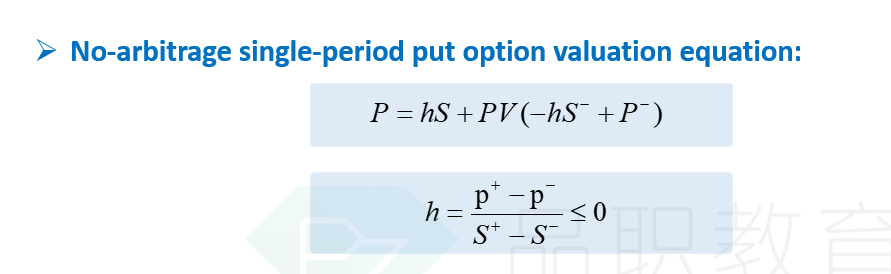

- 现在市场中的put option价格被高估,所以应该short put。但因为无套利需要满足两个条件:1.不承担任何风险,2.自己不出钱。Short put头寸在股票价格下跌时有亏损,所以需要再加上一个当股票价格下跌时可以带来收益的头寸,即short sell the underlying.

- 也可以从复制的角度出发,因为市场中的put被高估,所以short put。因为套利是买卖相同的东西,所以需要再复制一个put option的long头寸。long put头寸可以通过short sell the underlying 和lend a portion of the proceeds来实现。

老师我能判断出需要short put,但是不明白为什么还要long put,而且long put为什么相当于short underlying,这里的underlying特指stock吗?是否可以理解为asset?