NO.PZ2024061801000098

问题如下:

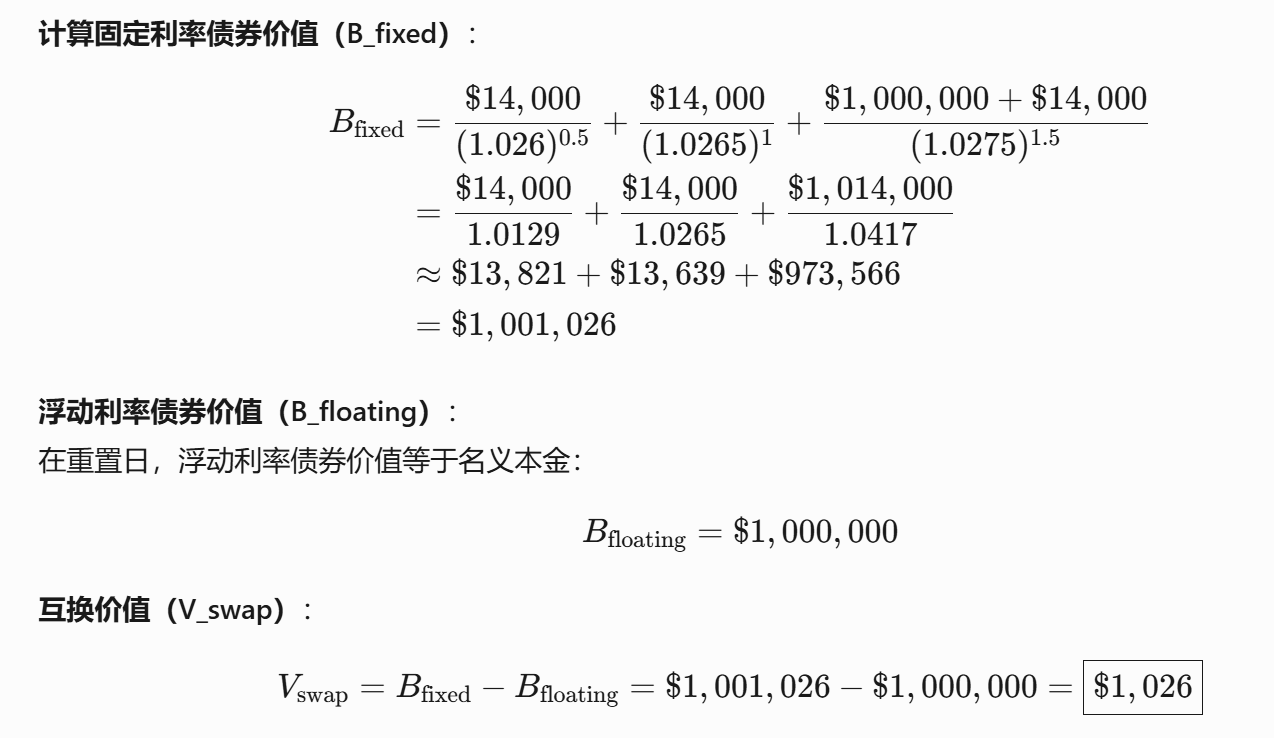

Consider the following information:

$1 million notional value, semiannual, 18-month maturity.

Spot SOFR rates: 6 months, 2.6%; 12 months, 2.65%; 18 months, 2.75%.

The fixed rate is 2.8%, with semiannual payments.

Which of the following amounts is closest to the value of the swap to the floating rate payer, assuming that it is currently the floating-rate reset date?

选项:

A.−$1,026.

B.$1,026.

−$12,416.

D.$12,416.

解释:

但為什麼這題不是用e計算??是因為SOFR嗎?

之前做其他相似題目,例如下面這題是也用e計算。swap 不是都用e計算嗎?