15:54 (1.5X)

吴昊_品职助教 · 2025年05月02日

嗨,爱思考的PZer你好:

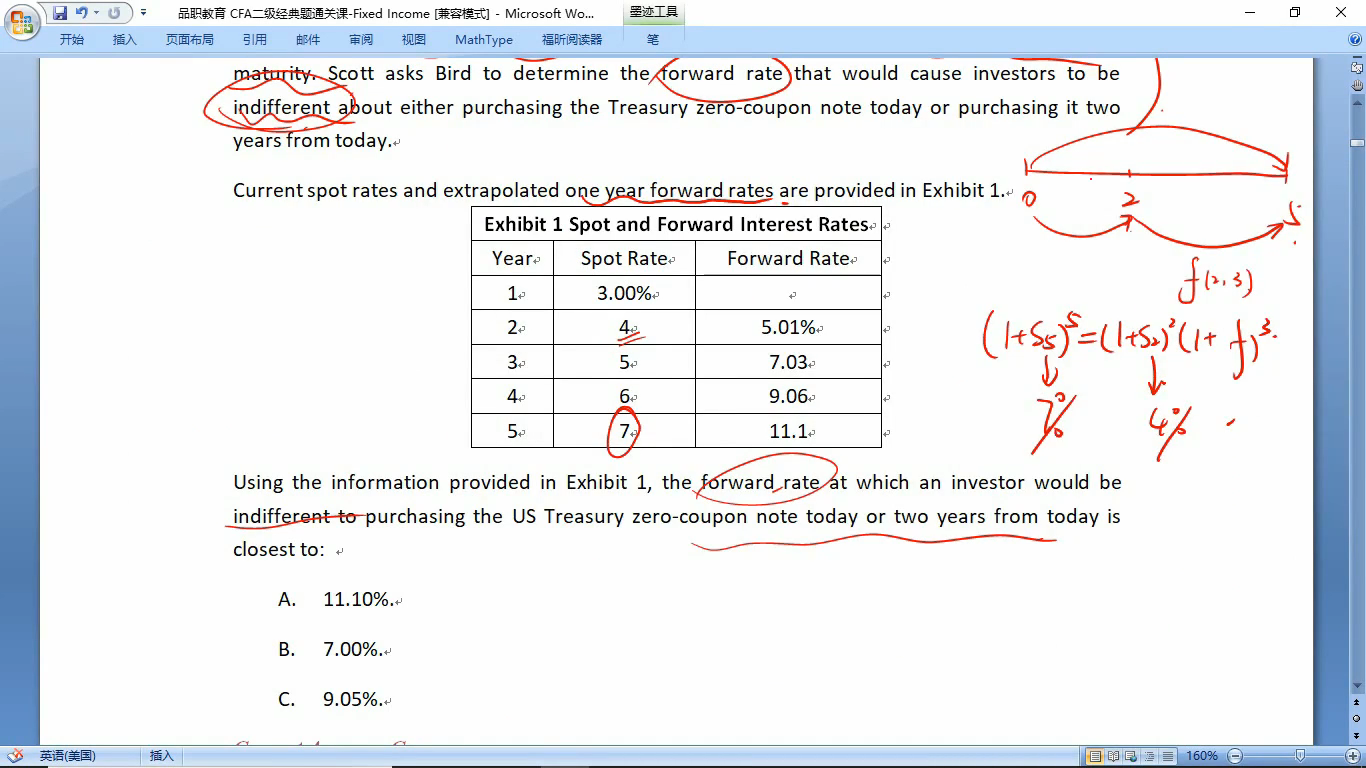

Scott says that some investors may purchase this Treasury zero-coupon note today and hold it for five years to maturity. Scott continues by stating that other investors may purchase this Treasury zero-coupon note in two years and then hold it for three years to maturity.

有些投资者会在现在买五年期的零息债券,另外一些投资者会在两年之后买零息债券并且持有三年。现在要求这两种投资方式无差别时的forward rate。可以通过殊途同归来列式,得到:

(1+S5)^5=(1+S2)^2×[1+f(2,3)]^3,这里的f(2,3)代表的就是第二年开始,三年期的远期利率,也就是2到5的远期利率。

----------------------------------------------

加油吧,让我们一起遇见更好的自己!