NO.PZ2025042401000060

问题如下:

The OAS of a callable bond is 75 basis points in a zero volatility environment. As interest rate volatility increases, the bond's OAS most likely:

选项:

A.decreases.

B.remains the same.

C.increases.

解释:

Solution

-

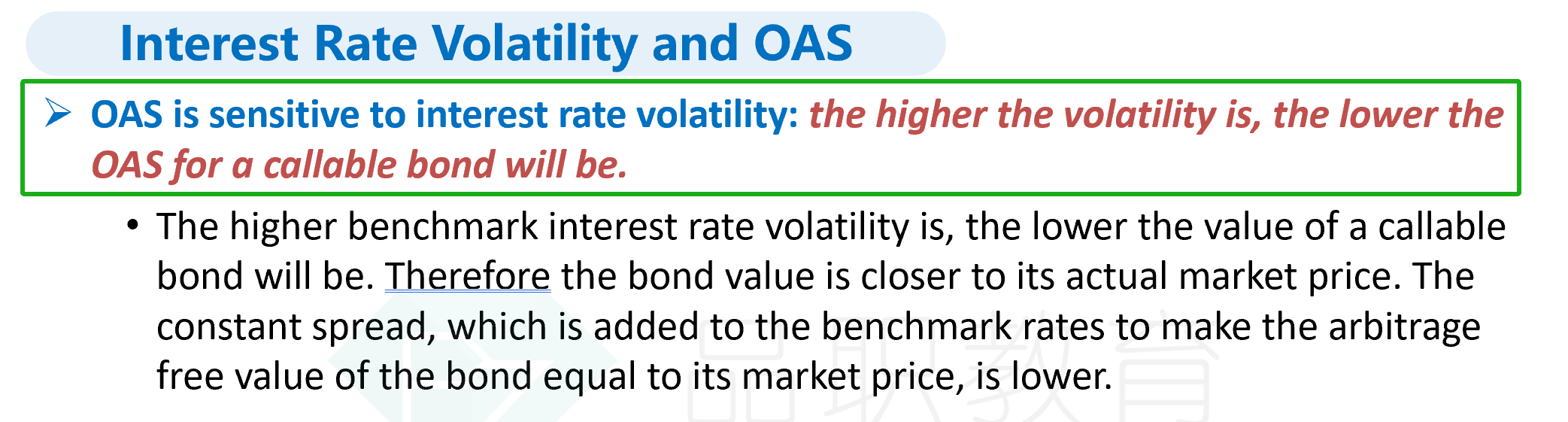

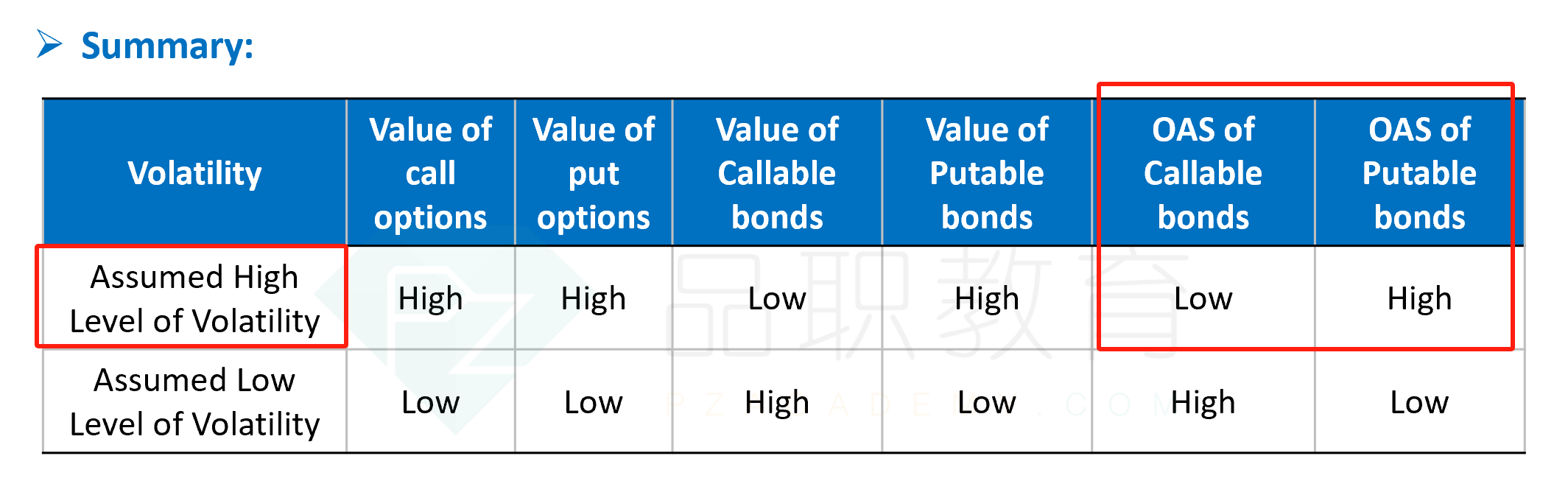

A is correct because as interest rate volatility increases, the OAS for the callable bond decreases.

-

B is incorrect because as interest rate volatility increases, the OAS for the callable bond decreases.

-

C is incorrect because as interest rate volatility increases, the OAS for the callable bond decreases.

- explain the calculation and use of option-adjusted spreads

OAS和callable,putable的关系。为什么选A