NO.PZ2023040501000022

问题如下:

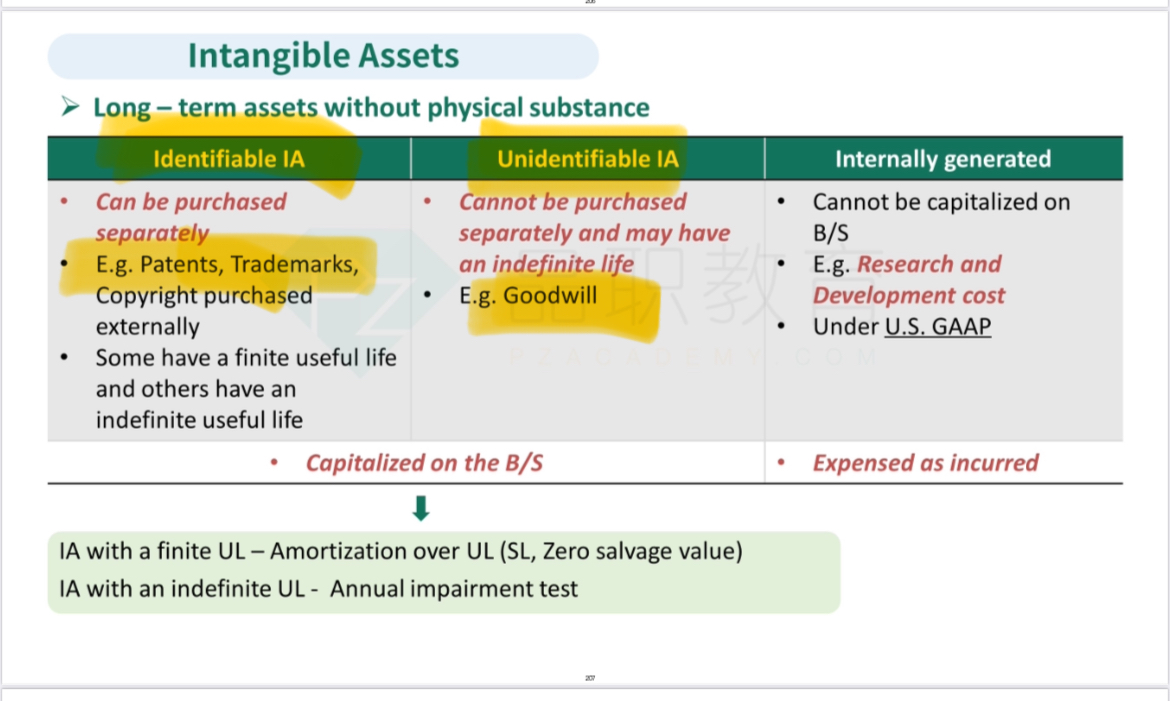

Finally, Treadway noted that during 2016 CCCL acquired 100% of MusicMusic (MM), a specialty cable music channel in an all-stock deal. At the time of the acquisition MM reported intangible assets for broadcast licenses at a value of $2,500. CCCL estimated the fair value of those licenses to be $5,500 at that date and estimated the value of the MusicMusic brand name to be $2,000, all figures in thousands. The acquisition did not give rise to any goodwill.

Before the calculation of amortization expense, the increase in CCCL’s intangible assets (in thousands) arising from the 2016 acquisition of MM is closest to:

选项:

A.$2,500.

$4,500.

$7,500.

解释:

CCCL acquired 100% of MM, therefore under IFRS it would use the acquisition method to account for the acquisition and the preparation of the consolidated financial statements. Under the acquisition method, CCCL would recognize the fair value of all of MM’s identifiable tangible and intangible assets regardless of whether or not they were recognized on MM’s balance sheet. Therefore, they would have added both the broadcast licenses and the brand name at fair value: $5,500 + 2,000 = $7,500.

在做合并的时候,对于可辨认公允净资产是要考虑这些商标,但不考虑商誉?