NO.PZ201812020100000102

问题如下:

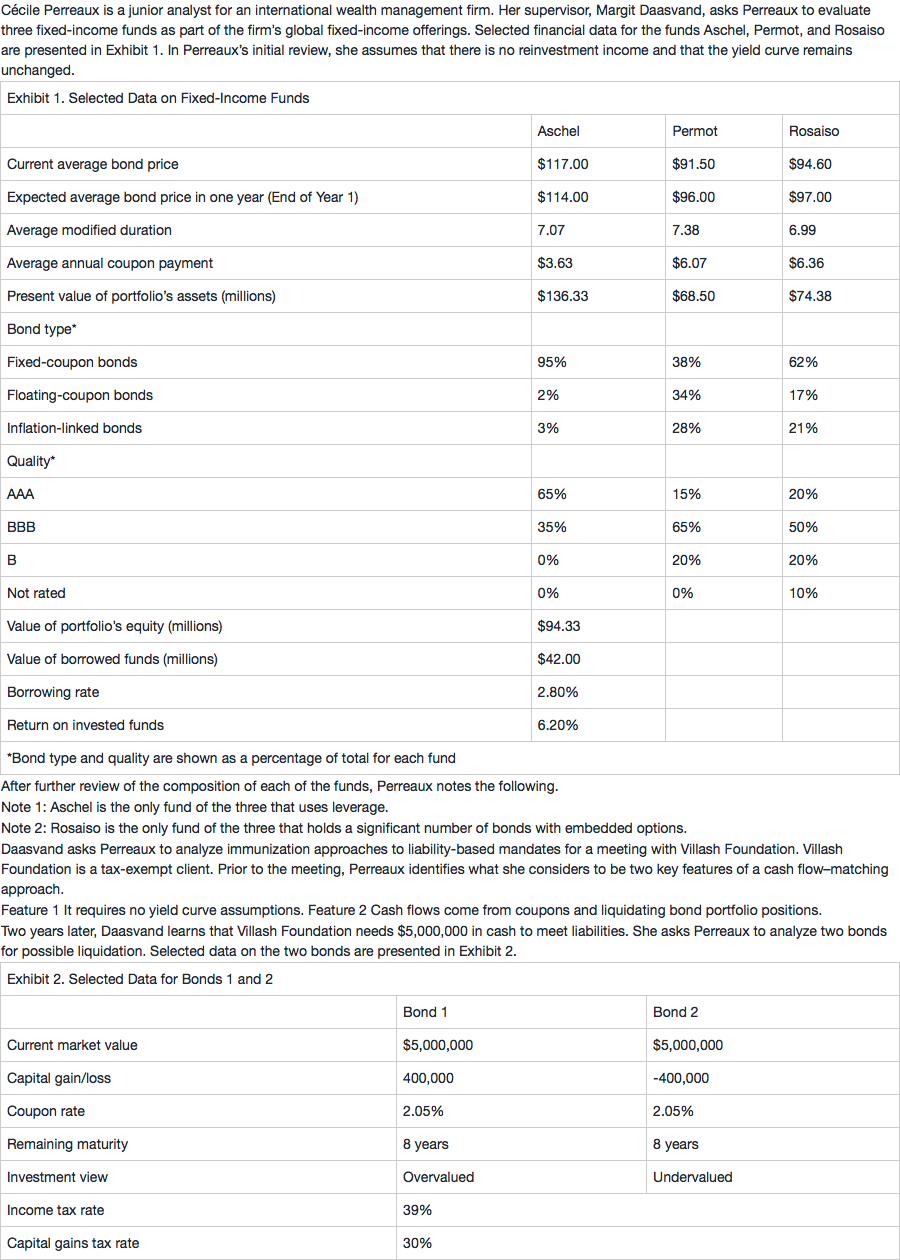

Cécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three fixed-income funds as part of the firm’s global fixed-income offerings. Selected financial data for the funds Aschel, Permot, and Rosaiso are presented in Exhibit 1. In Cécile’s initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

After further review of the composition of each of the funds, Cécile makes the following notes:

Note 1: Aschel is the only fund of the three that uses leverage.

Note 2: Rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.

Margit asks Cécile to analyze liability-based mandates for a meeting with Villash Foundation. Villash Foundation is a tax-exempt client. Prior to the meeting, Cécile identifies what she considers to be two key features of a liability-based mandate.

Feature 1 It matches expected liability payments with future projected cash inflows.

Feature 2 It can minimize the risk of deficient cash inflows for a company

Two

years later, Margit learns that Villash Foundation needs $5 million in

cash to meet liabilities. She asks Cécile to analyze two bonds for possible

liquidation. Selected data on the two bonds are presented in Exhibit 2.

Based on Exhibit 1, the rolling yield of Aschel over a one-year investment horizon is closest to:

选项:

A.–2.56%.

B.0.54%.

C.5.66%.

解释:

B is correct.

The rolling yield is the sum of the yield income and the rolldown return. Yield income is the sum of the bond’s annual current yield and interest on reinvestment income. Perreaux assumes that there is no reinvestment income for any of the three funds, and the yield income for Aschel will be calculated as follows: Yield income = Annual average coupon payment/Current bond price = $3.63/$117.00 = 0.0310, or 3.10%.

The rolldown return is equal to the bond’s percentage price change assuming an unchanged yield curve over the horizon period. The rolldown return will be calculated as follows:

Rolldown return = (Ending Bond Price - Beginning Bond Price) / Beginning Bond Price

Rolldown return = (114.00 - 117.00) / 117.00

Rolling yield = Yield income + Rolldown return = 3.10% – 2.56% = 0.54%

想问一下Current Bond Price和PV of portfolio's assets的区别是什么?