NO.PZ2024030503000196

问题如下:

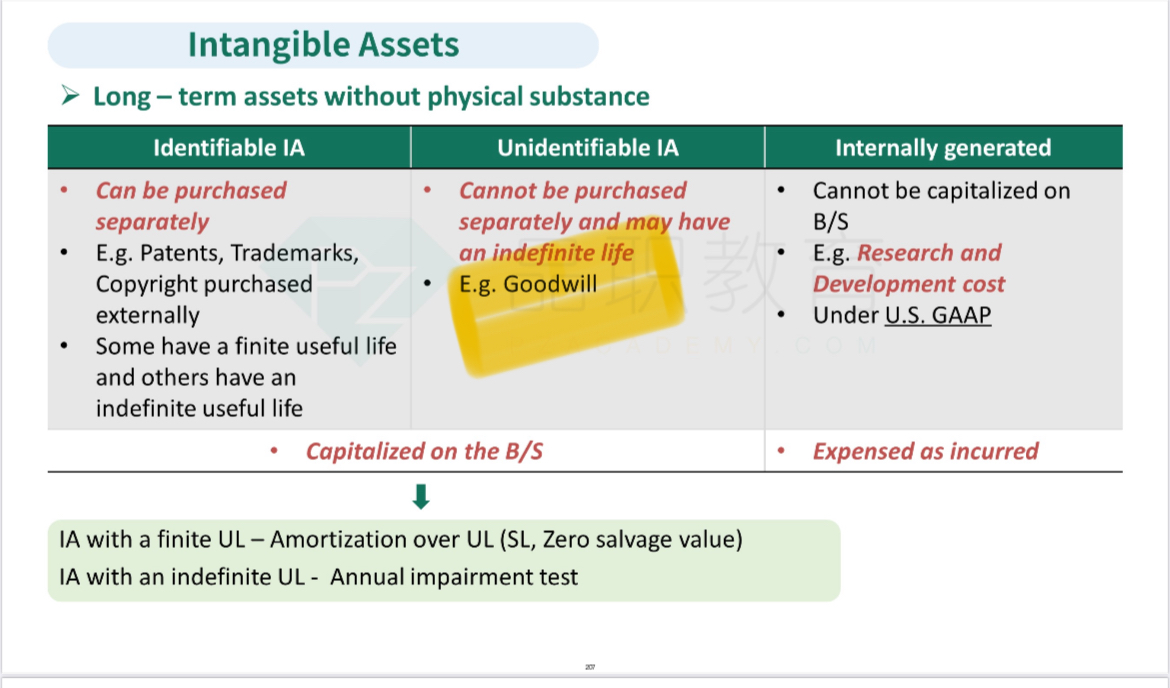

Question Accounting goodwill arising from acquisitions is:

选项:

A.expensed in the period it arises.

B.capitalized and amortized over a finite period.

C.capitalized and tested for impairment annually.

解释:

Solution-

Incorrect because under both IFRS and US GAAP, accounting goodwill arising from acquisitions is capitalized.

-

Incorrect because under both IFRS and US GAAP, accounting goodwill arising from acquisitions is capitalized. Goodwill is not amortised but is tested for impairment annually. If goodwill is deemed to be impaired, an impairment loss is charged against income in the current period.

-

Correct because under both IFRS and US GAAP, accounting goodwill arising from acquisitions is capitalized. Goodwill is not amortised but is tested for impairment annually. If goodwill is deemed to be impaired, an impairment loss is charged against income in the current period.

•

商誉在教材里面好像没有具体去讲,这个题的意思是什么