嗨,从没放弃的小努力你好:

同学,你好。

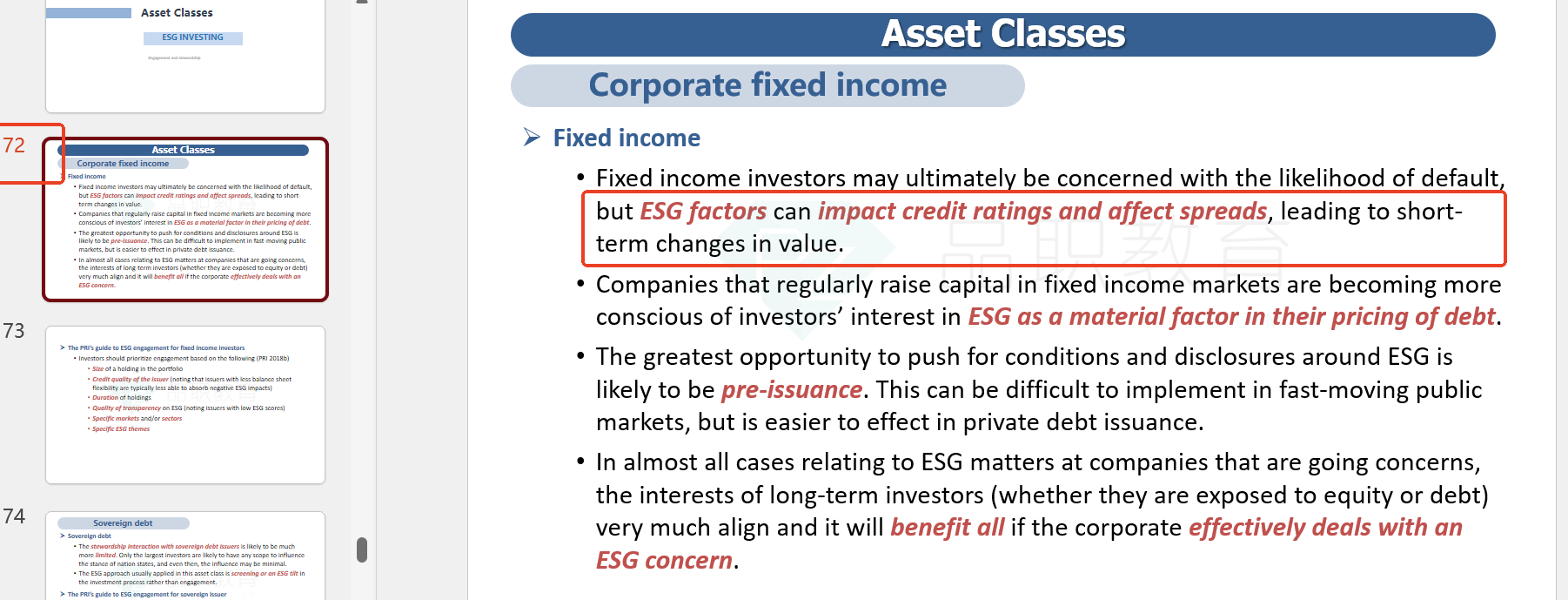

选项A在水印版讲义的第72页。明确提到 “ESG factors can affect both credit ratings and spreads, leading to short - term changes in value. Companies that regularly raise capital in fixed - income markets are becoming more conscious of investors’ interest in ESG as a material factor in their pricing of debt”,表明 ESG 因素会影响发行人的信用评级和债券利差,进而影响信用风险,这与选项 A 中 “ESG factors can affect credit risk at issuer level” 表述相符。

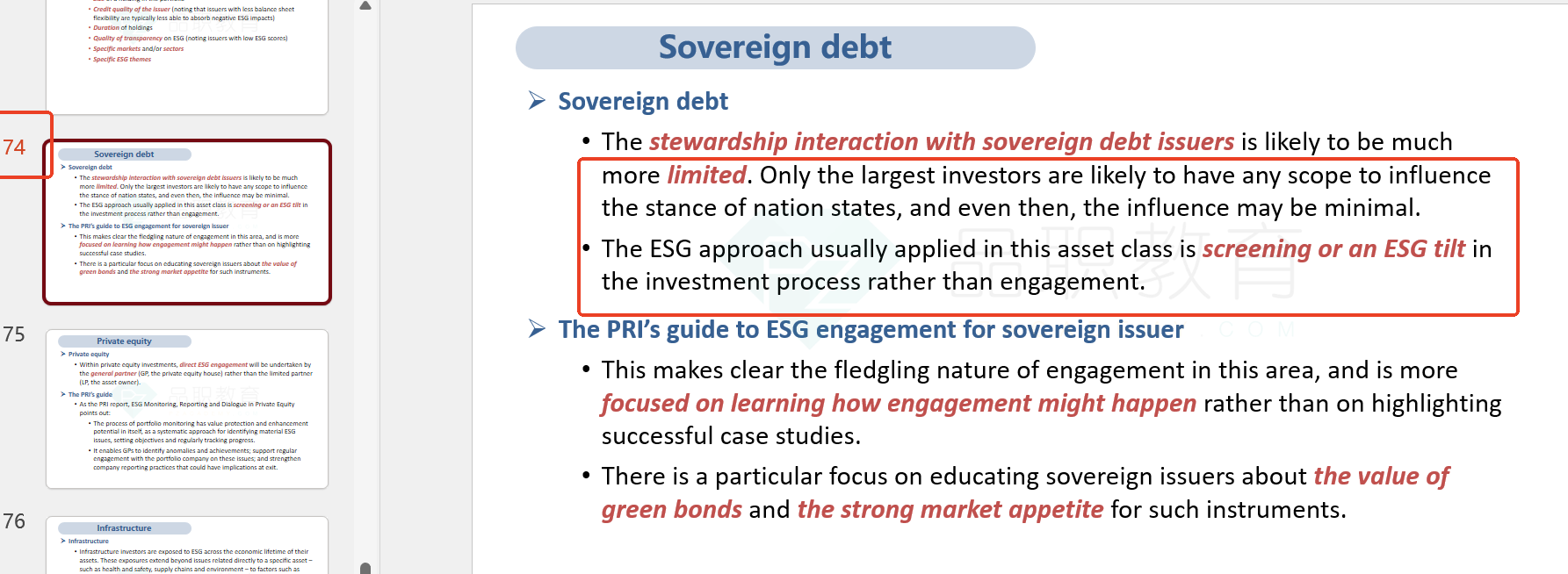

选项B在水印版讲义的第74页。与讲义中 “Sovereign debt...ESG approach usually applied in this asset class is screening or an ESG tilt in the investment process rather than engagement” 不符,主权债务投资者只是较少进行 ESG 参与,但并非不整合 ESG 因素。

选项C. Contingent liabilities are not captured in sovereign credit ratings.(或有负债不会被纳入主权信用评级)虽然没有在第六章出现。但是它的表述是错误的,因为主权信用评级通常会考虑 或有负债(Contingent Liabilities),特别是以下几种:

- 政府担保的债务(如国有企业债务、政府支持的银行债务)。

- 养老金负债(政府对养老金系统的隐性承诺)。

- 公共基础设施 PPP(Public-Private Partnership)项目的长期承诺。

- 灾害应对成本(如极端天气事件导致的财政支出压力)。

例如:

- 标普(S&P) 在主权信用评级模型中明确考虑或有负债的规模和可能性。

- 穆迪(Moody’s) 也会评估财政赤字、政府债务、以及隐性债务的影响。

----------------------------------------------

虽然现在很辛苦,但努力过的感觉真的很好,加油!