NO.PZ2023091601000018

问题如下:

The CIO of a global macro fund is assessing the performance of the

international portfolio managers of the fund. The CIO gathers the annualized

total returns of a sample of the managers as presented in the following table:

The CIO calculates

the central moments of these returns. What is the correct unbiased sample

variance of the returns data?

选项:

A.0.00128

0.00160

0.00288

0.00360

解释:

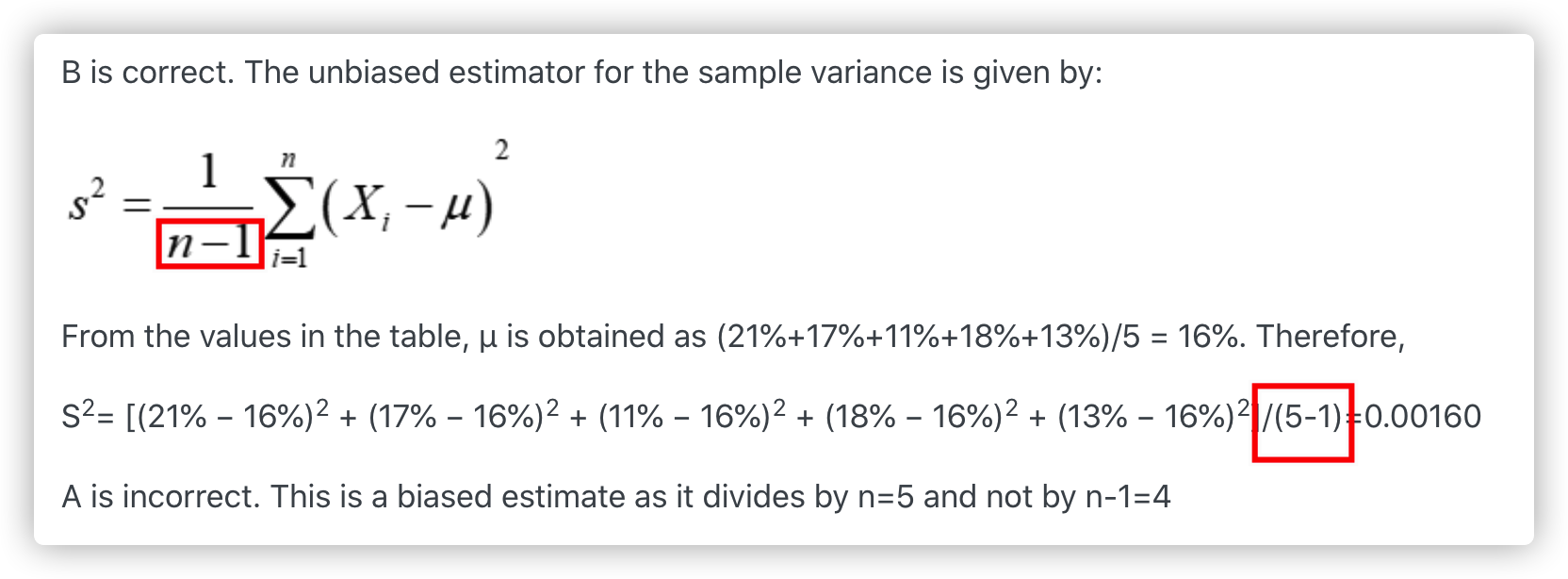

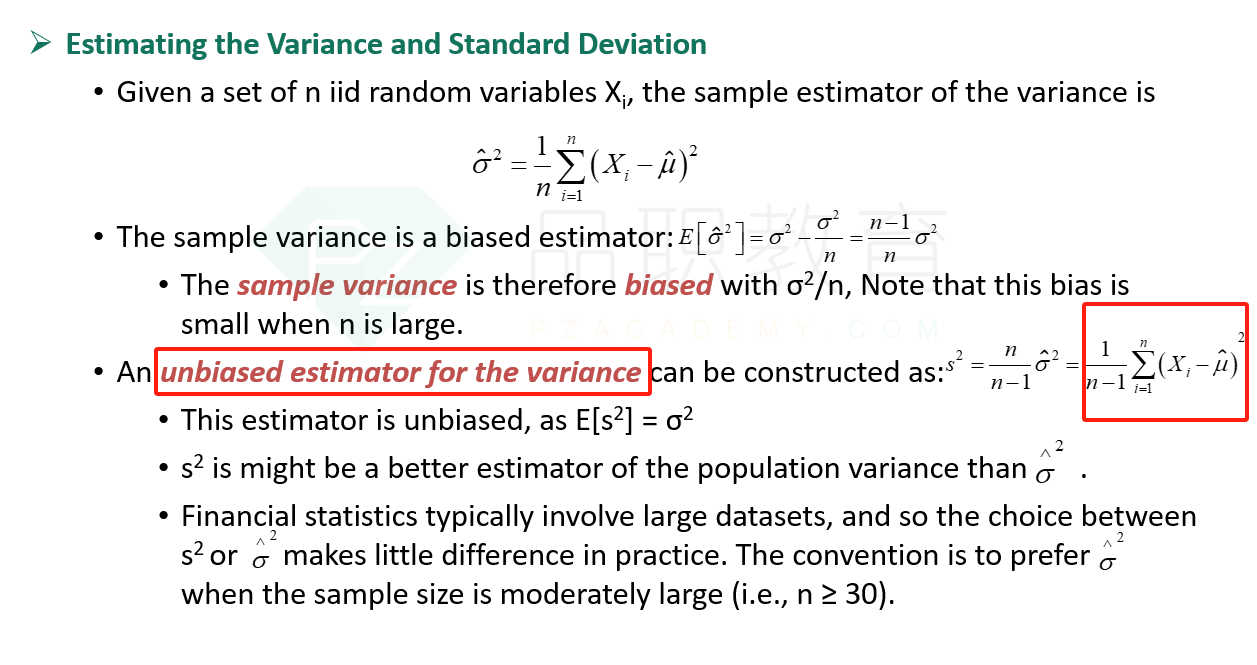

B is correct. The

unbiased estimator for the sample variance is given by:

From the values in

the table, μ is obtained as (21%+17%+11%+18%+13%)/5 = 16%. Therefore,

S2=

[(21% − 16%)2 + (17% − 16%)2 + (11% − 16%)2 +

(18% − 16%)2 + (13% − 16%)2]/(5-1)=0.00160

A is incorrect.

This is a biased estimate as it divides by n=5 and not by n-1=4

C is incorrect.

This uses a μ that is adjusted with n-1, resulting in 20%, while also dividing

the numerator of the sample estimator by 5 and not 4.

D is incorrect.

This uses a μ that is adjusted with n-1, resulting in 20%.