NO.PZ2017092701000013

问题如下:

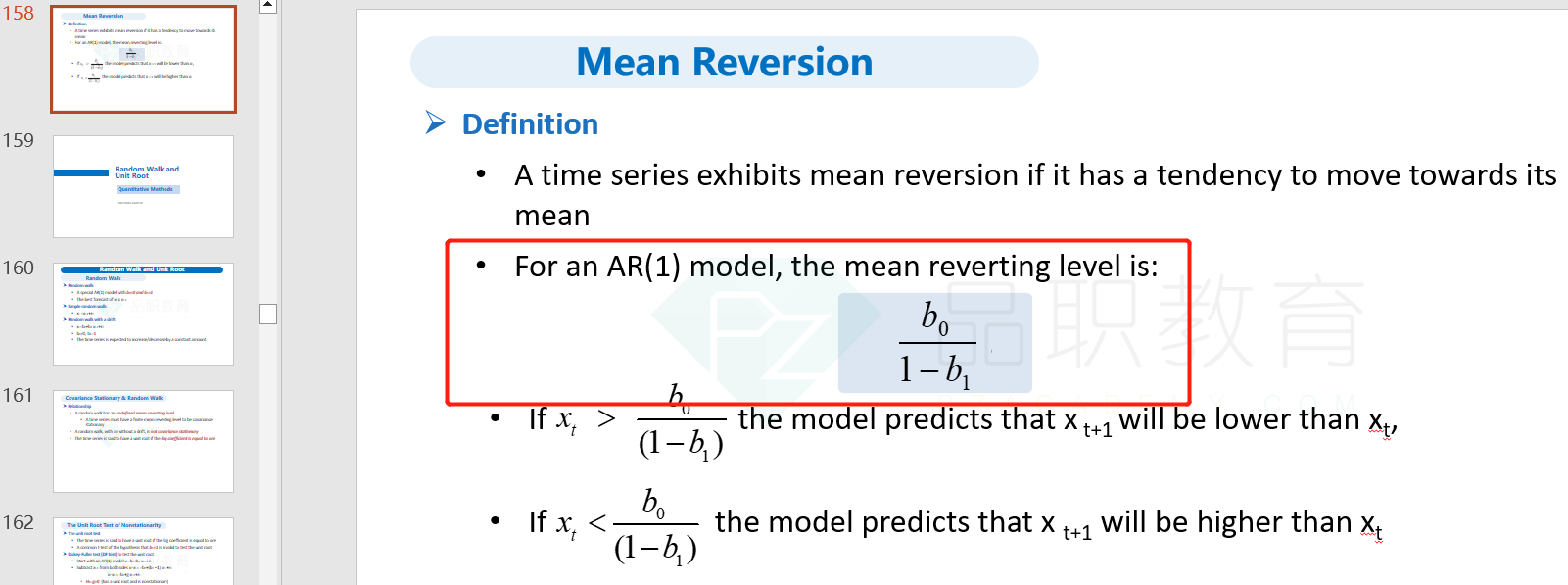

Assume that changes in the civilian unemployment rate are covariance stationary and that an AR(1) model is a good description for the time series of changes in the unemployment rate. Specifically, we have ΔUERt = −0.0668 − 0.2320ΔUERt−1(using the coefficient estimates given in the previous problem). Given this equation, what is the mean-reverting level to which changes in the unemployment rate converge?

解释:

When a covariance-stationary series is at its mean-reverting level, the series will tend not to change until it receives a shock (εt). So, if the series ΔUERt is at the mean-reverting level, ΔUERt = ΔUERt−1. This implies that ΔUERt= −0.0668 −

0.2320ΔUERt, so that (1 + 0.2320)ΔUERt= −0.0668 and ΔUERt

= −0.0668/(1 + 0.2320) = −0.0542. The mean-reverting level is −0.0542. In an AR(1) model, the general expression for the mean-reverting level is b0/(1 − b1).

这个考点在讲义哪里?跟那个单位根有联系吗?