这个题没读懂,我读出来的意思是哪一个credit-related risk,但是liquidity risk不是credit-related呀?

问题如下图:

选项:

A.

B.

C.

解释:

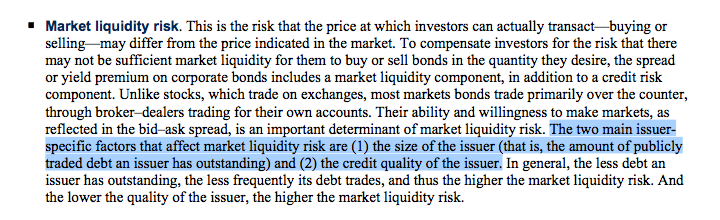

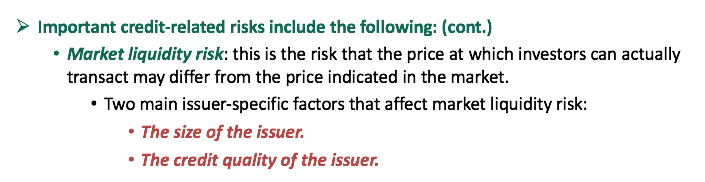

NO.PZ2018062020000010 fault risk. Market liquity risk. C is correct. Liquity risk reflects the fferenbetween the market prianactually trang price. Investors neeto ppremiums when securities lacks transactions.什么是cret relaterisk

老师,为什么不选A呢?应该选自身的risk更准确吧

请问A为什么不对呢?