NO.PZ2022081802000035

问题如下:

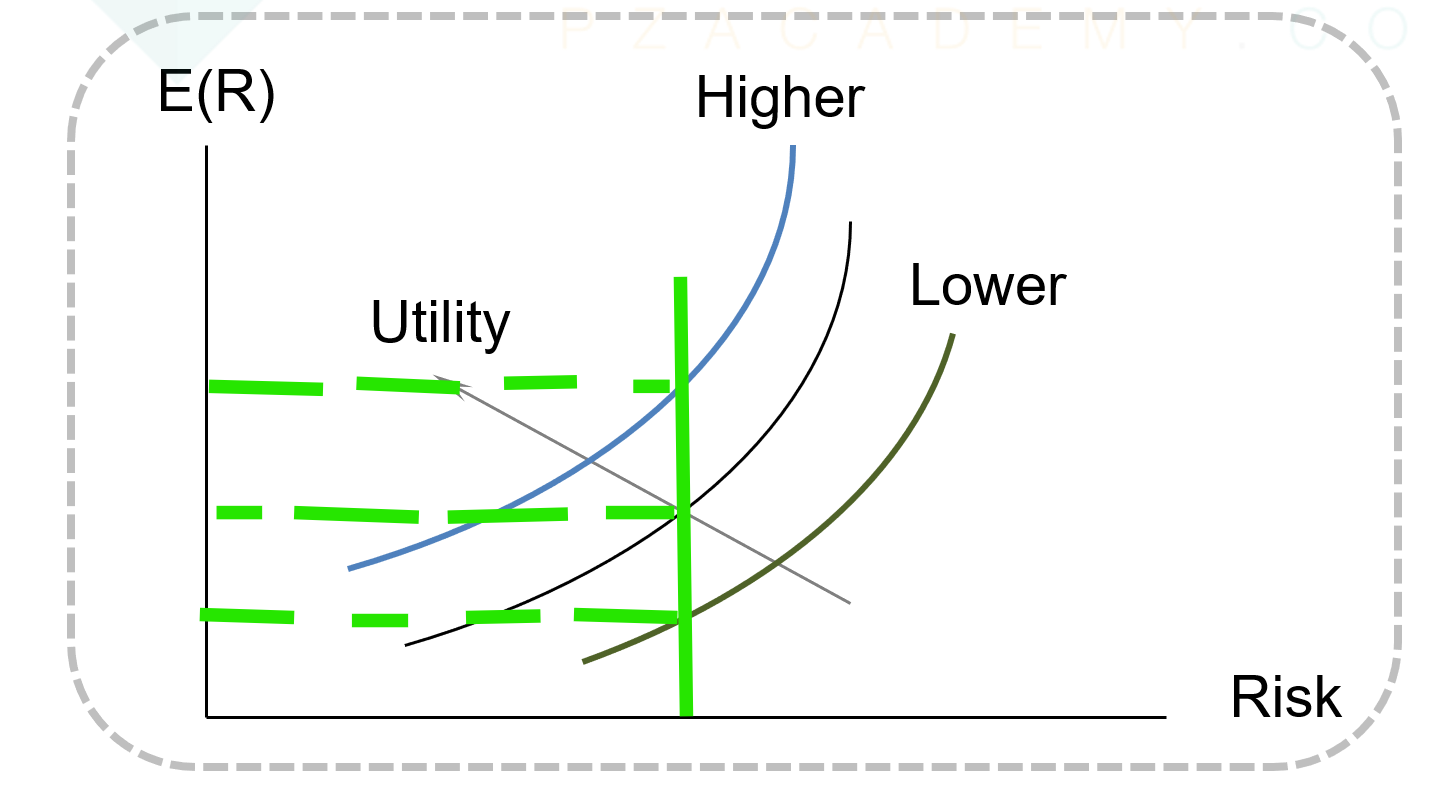

Question If Investor A has a lower risk aversion coefficient than Investor B, on the capital allocation line, will Investor B’s optimal portfolio most likely have a higher expected return?选项:

A.Yes B.No, because Investor B has a higher risk tolerance C.No, because Investor B has a lower risk tolerance解释:

SolutionC is correct. Investor B has a higher risk aversion coefficient, thus a lower risk tolerance and a lower expected return on the capital allocation line.

A is incorrect. Investor A has a higher expected return on the capital allocation line.

B is incorrect. Investor B has lower risk tolerance.

根据utility公式,B更厌恶风险,expected return 更高才对,CAL上远离Rf么