NO.PZ2024042601000030

问题如下:

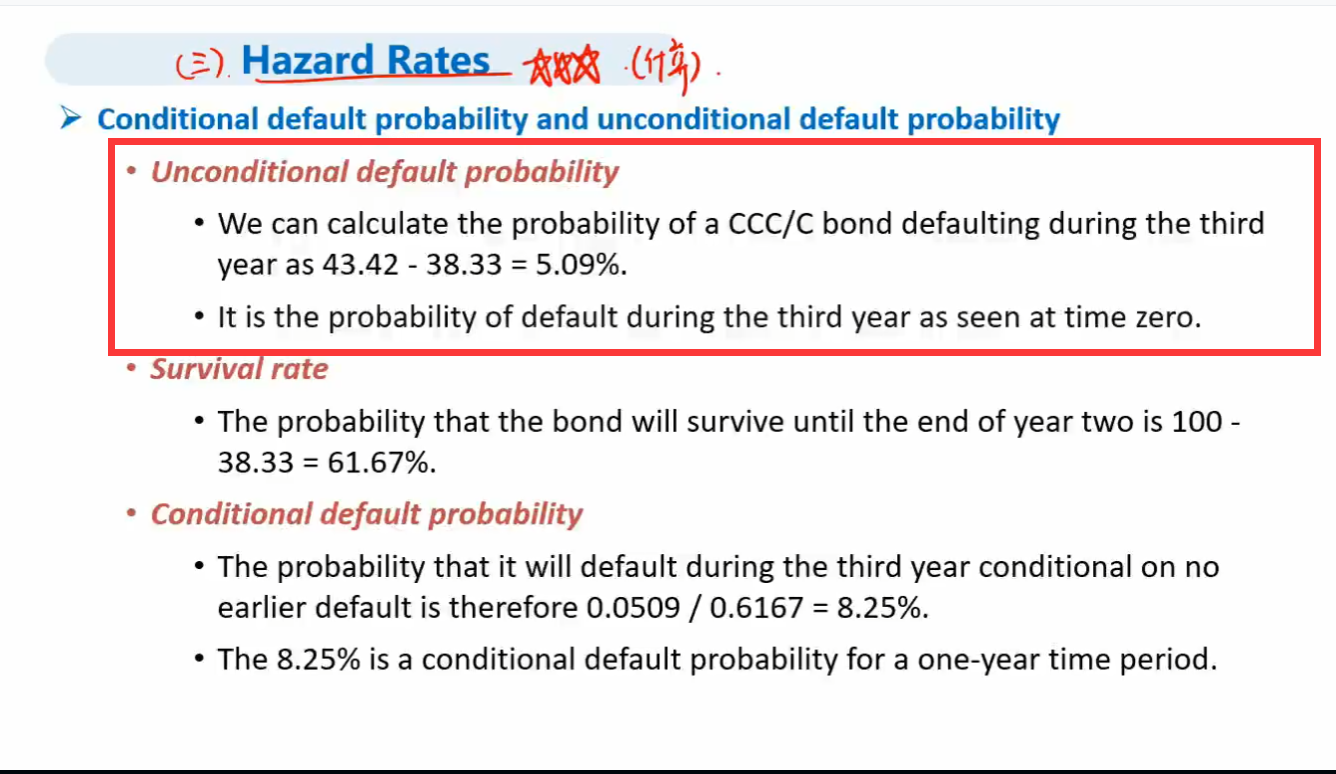

Suppose the hazard rate is constant and equal to 0.090. In this case, each of the following is true except which is false?

选项:

A.The unconditional one-year default probability is 8.6%

The unconditional two-year default probability is 16.5%

The probability of joint event of survival through the first year and default in the second year is 7.9%

The conditional one-year default probability, given survival through the first year, is 17.3%

解释:

The conditional one-year PD is equal to 8.6%, same as the unconditional one-year default probability.

请问老师,选项B The unconditional two-year default probability is 16.5%,为什么是算cumulativePD呢?unconditional PD是两期survival rate相减,不是吗?