请问unconditional expected value of the variance of 0.0001是怎么算出来的?为什么estimated variance at time t-1 was 0.0004会等于0.022? The deviation 1.9849%是怎么算出来的?谢谢!

笛子_品职助教 · 2024年08月12日

嗨,从没放弃的小努力你好:

unconditional expected value of the variance of 0.0001是怎么算出来的?

Hello,亲爱的同学~

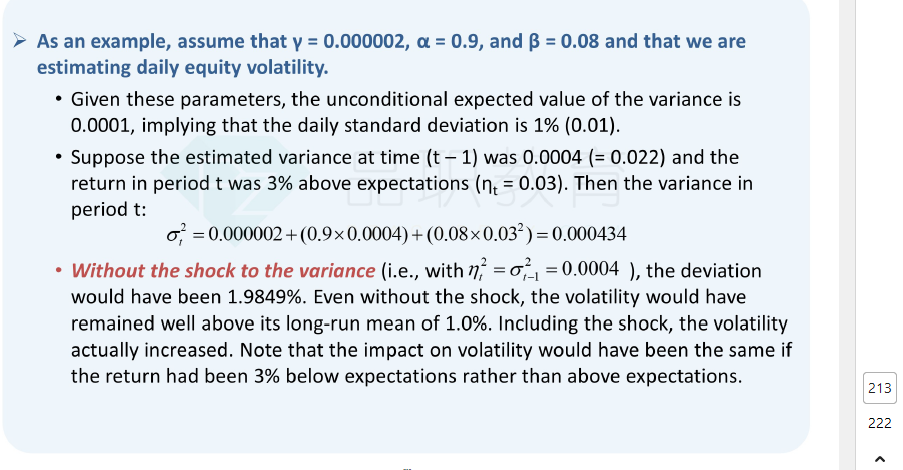

同学问的这道题,是基础讲义213页的例题。

1)unconditional expected value of the variance的公式:

2)把数字 代入上述背诵的公式:

代入上述背诵的公式:

0.000002 / (1-0.9 - 0.08) = 0.00001

为什么estimated variance at time t-1 was 0.0004会等于0.022?

estimated variance at time t-1 was 0.0004是已知条件。

0.022这里是印刷错误。

0.022应该印刷为0.02的平方,后面一个2应放到右上角,表示标准差是0.2。

The deviation 1.9849%是怎么算出来的?谢谢!

1) 没有shock的时候,公式为:

2)带入数字:0.000002 + (0.98)*0.0004 = 0.000394

0.000394是方差,0.000394开平方根是标准差,标准差 = 0.019849

同学注意要使用公式。

解析里的 是近似值。精确值不是0.0004,是用算出来的0.000394。

是近似值。精确值不是0.0004,是用算出来的0.000394。

----------------------------------------------

加油吧,让我们一起遇见更好的自己!