NO.PZ2024021803000008

问题如下:

What is the closest price to a nine-month call option on a non-dividend-paying stock with an exercise price of £47, given a forward contract priced at £50, an annual risk-free rate of 10% and a nine-month put option on the stock with an exercise price of £47 trades at £4?选项:

A.£6.79 B.£7.22 C.£7.30解释:

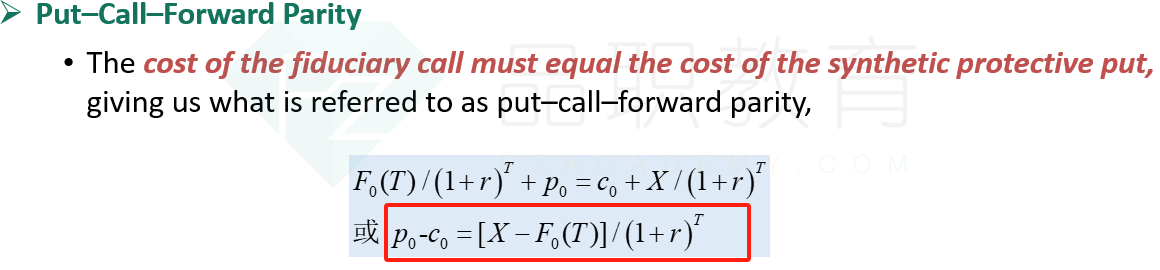

Put-call forward parity relates the prices of puts, calls, and forward contracts under no arbitrage conditions. 使用无套利条件下的看涨看跌远期平价关系,可以联系看跌期权、看涨期权和远期合约的价格。根据put-call-forward parity,带入数值计算:c=4+50/1.19/12-47/1.19/12=6.79.

老师能具体解释一下这个部分吗 50/1.19/12-47/1.19/12?