20:48 (2X)

这里是否可以不用公式计算convexity,直接说with similar duration, the portfolio with the smallest dispersion have the smallest convexity, and then smallest structural risk, which is portfolio B

发亮_品职助教 · 2024年08月07日

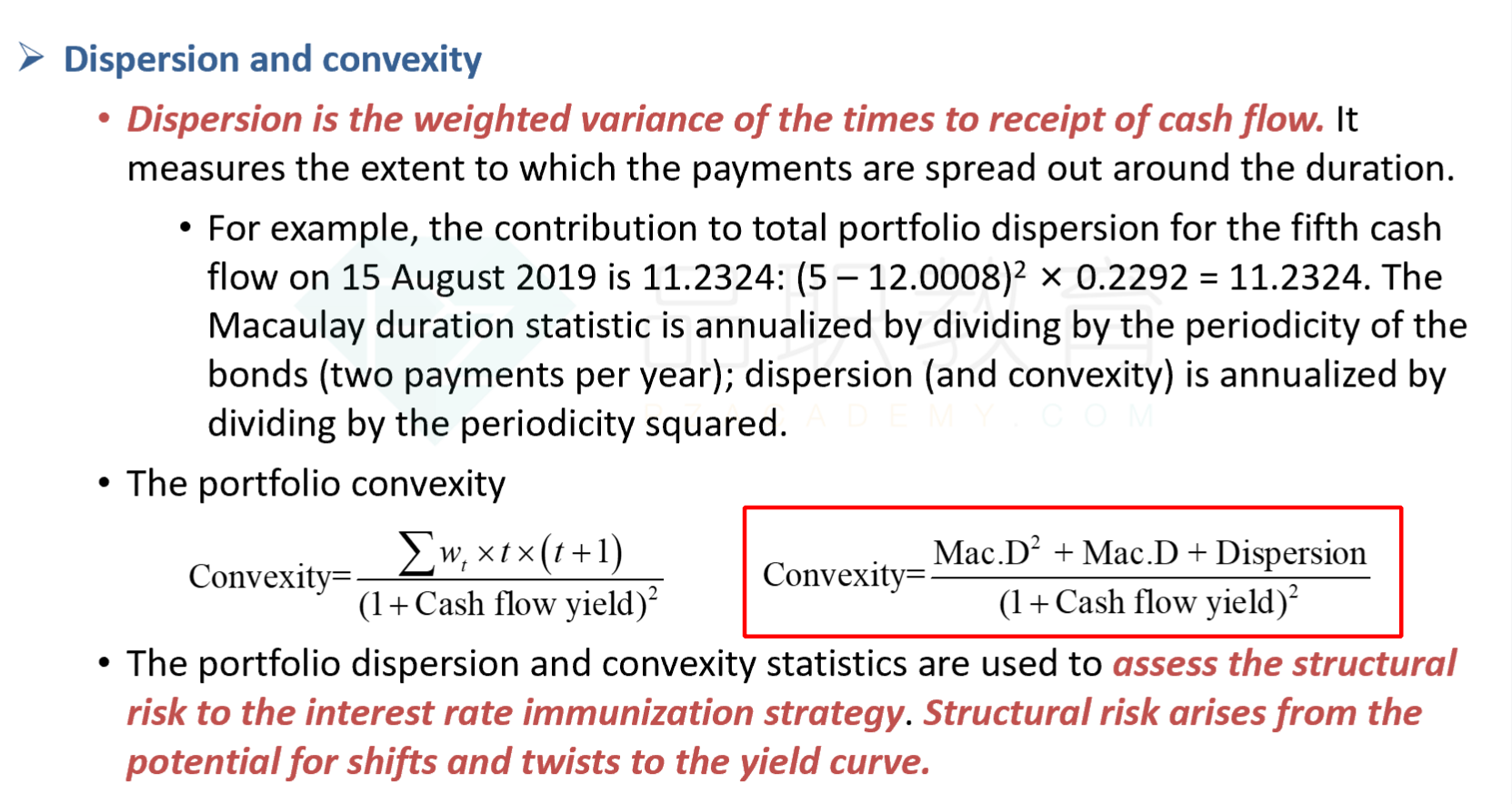

公式有,参考基础班讲义88页:

直接说with similar duration, the portfolio with the smallest dispersion have the smallest convexity, and then smallest structural risk, which is portfolio B

这道题还不行。因为影响convexity的数据,除了macaulay duration之外,还有cash flow yield。以上2个指标保持一致的情况下,才可以说现金流越分散的组合,其convexity越大。

这道题的数据虽然三个组合的macaulay duration差不多大,但是cash flow yield差距有点大,而且cash flow yield是在公式的分母上,一点点差距就会使得最终计算结果差异被放大。

这道题只能拿公式算。因为以前真题考过这个公式计算,所以出这道题的目的就是想让大家训练一下公式。

如果题目说三个组合macaulay duration和cash flow yield差不多大,这时候可以不用公式计算,直接说以下就是OK的:

with similar duration and cash flow yield, the portfolio with the smallest dispersion have the smallest convexity, and then smallest structural risk, which is portfolio B