NO.PZ2023090801000007

问题如下:

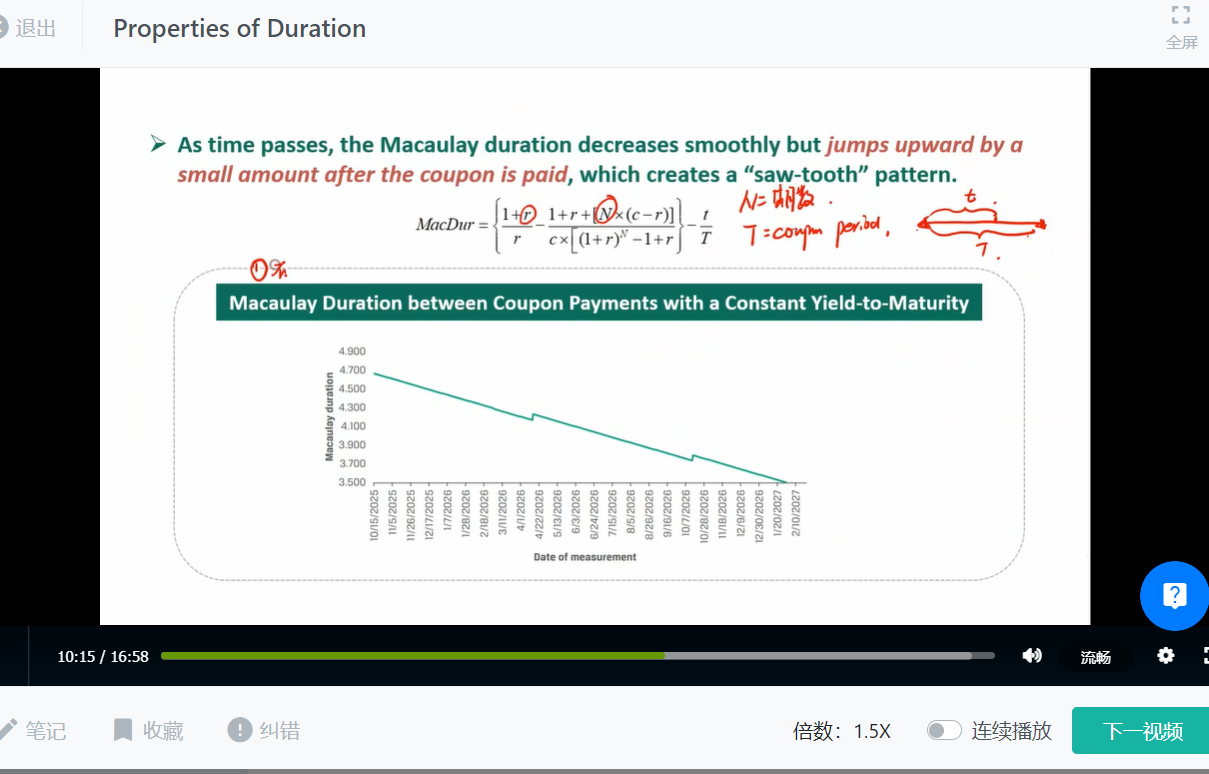

Between coupon payments, if the yield-to-maturity does not change, the Macaulay duration of a bond:

选项:

A.

decreases throughout the coupon period.

B.

is constant throughout the coupon period.

C.

increases throughout the coupon period.

解释:

A is correct. During the coupon period, the Macaulay duration declines smoothly until the next coupon period, at which time it jumps.

请问这题题目和知识点如何理解?