问题如下图:没明白,求解释,谢谢。。。

选项:

A.

B.

C.

解释:

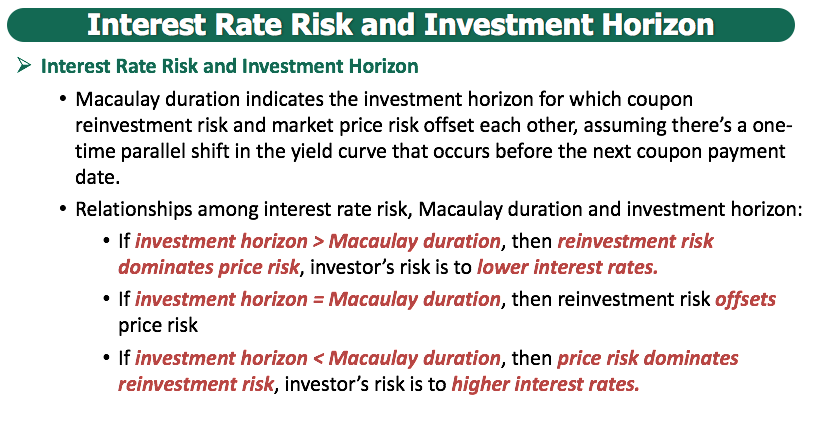

NO.PZ2016031001000130 问题如下 The holng periofor a bonwhithe coupon reinvestment risk offsets the market pririsk is best approximateby: A.ration gap. B.mofieration. C.Macaulration. C is correct.When the holr of a bonexperiences a one-time parallel shift in the yielcurve, the Macaulration statistic intifies the number of years necessary to holthe bonso ththe losses (or gains) from coupon reinvestment offset the gains (or losses) from market prichanges. The ration gis the fferenbetween the Macaulration anthe investment horizon. Mofieration approximates the percentage prichange of a bongiven a change in its yielto-maturity. 考点Interest Rate Risk Investment Horizon解析当再投资风险和市场风险相抵消的时候,也就是投资期等于麦考利久期。此时,两者之差是ation gap=0。题目问的是当两个风险相互抵消的时候,能够衡量投资期的是什么,所以我们选的是麦考利久期,故C正确。 为什么不选A,语言文字游戏?

NO.PZ2016031001000130 问题如下 The holng periofor a bonwhithe coupon reinvestment risk offsets the market pririsk is best approximateby: A.ration gap. B.mofieration. C.Macaulration. C is correct.When the holr of a bonexperiences a one-time parallel shift in the yielcurve, the Macaulration statistic intifies the number of years necessary to holthe bonso ththe losses (or gains) from coupon reinvestment offset the gains (or losses) from market prichanges. The ration gis the fferenbetween the Macaulration anthe investment horizon. Mofieration approximates the percentage prichange of a bongiven a change in its yielto-maturity. 考点Interest Rate Risk Investment Horizon解析当再投资风险和市场风险相抵消的时候,也就是投资期等于麦考利久期。此时,两者之差是ation gap=0。题目问的是当两个风险相互抵消的时候,能够衡量投资期的是什么,所以我们选的是麦考利久期,故C正确。 看了解析及其他人的提问,也明白二者相互抵消的时候ration g =0, 还是不明白为什么麦考利久期就可以衡量呢??

当gap=0的时候,不就是相等的时候吗,为什么不选A

holng perio是持有期的意思吗?并不是再投资期限意思啊

该知识点在哪个视频?还是理解得不透彻。求讲解知识点。