NO.PZ202208260100000706

问题如下:

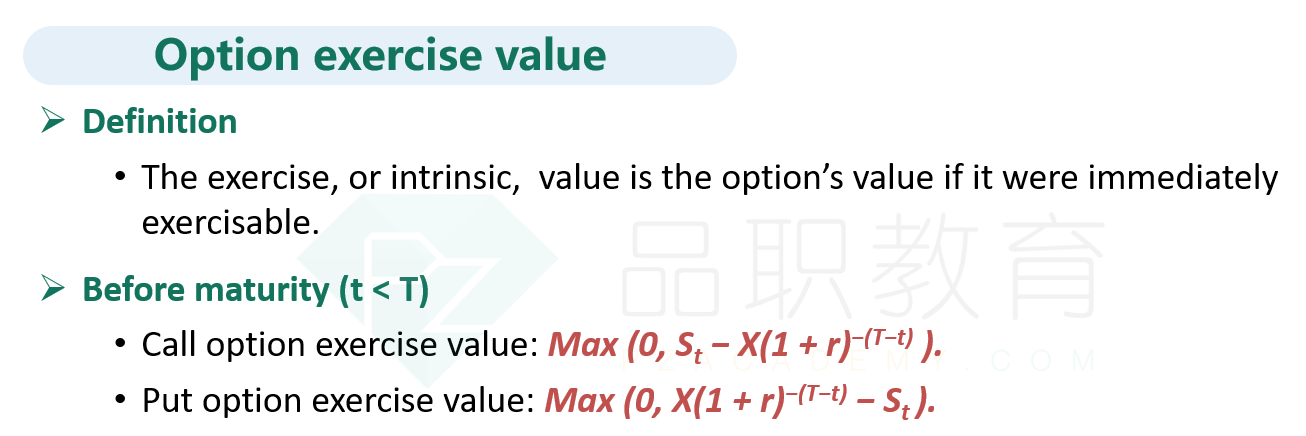

Which of the following statements correctly describes the put option and call option premiums given the relationship between Biomian’s current price of INR 295 and the exercise price equal to the forward price of INR 300.84?

选项:

A.The call option’s premium consists solely of time value, and the put option’s premium consists solely of exercise value.

B.The call option’s premium consists solely of exercise value, and the put option’s premium consists solely of time value.

C.The call option’s premium consists solely of time value, and the put option’s premium consists solely of time value.

解释:

C is correct. The exercise value of both the call and put options are zero because the present value of the exercise price is INR 295, which is equivalent to the stock price of INR 295. Thus, both option premiums reflect time value only. A is incorrect as this statement does not properly account for the discounting of the exercise price. B is incorrect as the call option’s premium does not reflect exercise value.

解析没有看明白,执行价格是300.84吗?为什么只有时间价值了?这个时间价值怎么理解。