NO.PZ202403050400001406

问题如下:

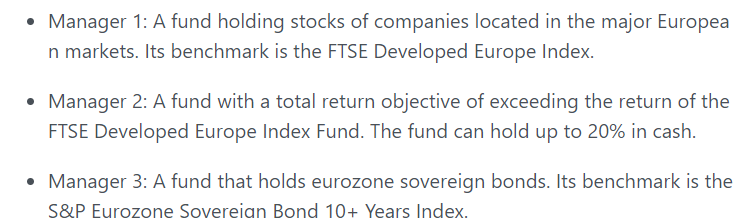

Lange is least likely to use the Sharpe ratio to evaluate the ex post portfolio returns of:

选项:

A.Manager 1.

B.Manager 2.

C.Manager 3.

解释:

A is incorrect because Portfolio A has neither cash nor leverage as a component of its investment decisions.

B is correct. The Sharpe ratio is unaffected by the addition of cash or leverage in a portfolio and would thus not be appropriate to evaluate a portfolio in which an allocation to cash was a key part of the investment decision process.

C is incorrect because Portfolio C has neither cash nor leverage as a component of its investment decisions.

不懂这题对应题干哪些信息