NO.PZ2024030508000065

问题如下:

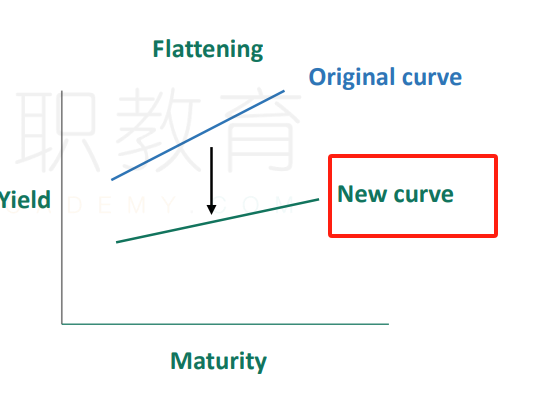

A fixed-income trader expects a bull flattening of the interest rate term structure, and wants to pursue a strategy that would profit from this movement in rates. The trader decides to achieve this goal by taking positions in 2-year and 10-year bonds. Will the 2-year rate increase or decrease in the trader’s expected scenario, and which of the following sets of trades would be the most likely to generate a profit if the trader’s expectations materialize?

选项:

A.2-year rate Decrease; Short the 2-year and buy the 10-year

B.

2-year rate Decrease; Buy the 2-year and short the 10-year

C.2-year rate Increase; Short the 2-year and buy the 10-year

D.2-year rate Increase; Buy the 2-year and short the 10-year

解释:

Explanation: A is correct. A bull flattening occurs when long-and short-maturity rates both move down, but long-maturity rates move down by more than short-maturity rates. If the trader expects a bull flattening, the trader can buy the 10-year bonds and short the 2-year bonds. If the trader is right, the 10-year bonds will increase in value relative to the 2-year bonds, and the trader will make money.

B, C, and D are incorrect.

Learning Objective: Define the “flattening” and “steepening” of rate curves and describe a trade to reflect expectations that a curve will flatten or steepen.

Reference: Global Association of Risk Professionals, Valuation and Risk Models (New York, NY: Pearson, 2023). Chapter 10. Interest Rates [VRM–10]

请老师讲解一下这道题