NO.PZ202401170100001101

问题如下:

Which of Anderson’s three statements regarding hedge fund strategies is correct?选项:

A.Statement 1 B.Statement 2 C.Statement 3解释:

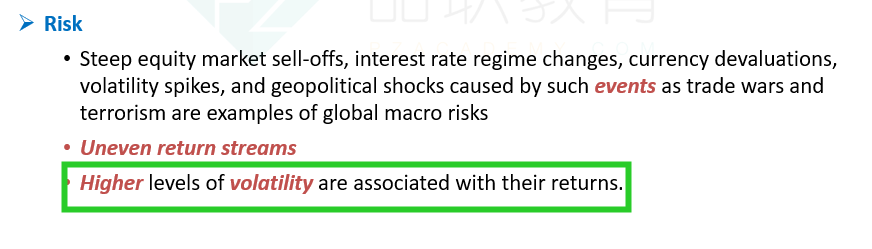

C is correct. Global macro investing may introduce natural benefits of asset class

and investment approach diversification, but they come with naturally higher

volatility in the return profiles typically delivered. The exposures selected in any

global macro strategy may not react to the global risks as expected because of

either unforeseen contrary factors or global risks that simply do not materialize;

thus, macro managers tend to produce somewhat lumpier and more uneven

return streams than other hedge fund strategies

详细解释一下,A,B,C