NO.PZ202209060200004703

问题如下:

Based on the data in Exhibit 2, will the client discussed most likely be able to immunize its DB plan given the interest rate scenario described by Silver?选项:

A.Yes B.No, because of the differences in money duration C.No, because of the differences in convexity and dispersion解释:

SolutionC is correct. The money duration of the assets and liabilities are equal: 517,342,000 × 12.66 = 6,548,381,000, and 500,000,000 × 13.10 = 6,548,381,000. For parallel changes, the equal money durations and PV01 imply that assets and liabilities would move in tandem. Silver expects a bear steepener; that is, long rates will rise faster than short rates. In a bear steepener, long rates rise faster than short rates in a non-parallel fashion. Given that the assets have lower convexity and dispersion than the liabilities, they will underperform; that is, the liabilities would change by a greater amount than the assets.

A is incorrect because Silver expects a bear steepener; that is, long rates will rise faster than short rates. In a bear steepener, long rates rise faster than short rates in a non-parallel fashion. Given that the assets have lower convexity and dispersion than the liabilities, they will underperform.

B is incorrect because the differences in convexity and dispersion are unfavorable; that is, they are lower for the assets than for the liabilities. If the opposite were the case, then the liabilities would be immunized.

老师好,这道题我理解了,但是针对convexity的性质我突然有一点问题。

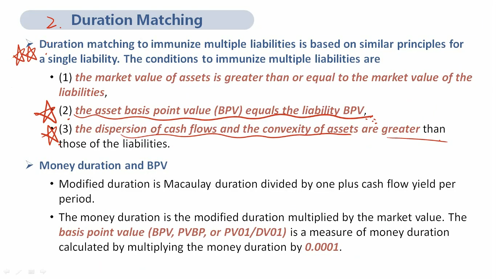

我记得上课的时候何老师讲过,针对multiple liability的immunization,我们要在asset的convexity大于liability的convexity的组合当中找convexity最小的那个,但是convexity不是越大越好么?因为convexity有涨多跌少的优点——那么这里为什么是要在大的convexity里面找投资组合最小的portfolio呢?

对应的知识点是基础班的这一页