NO.PZ2023041003000049

问题如下:

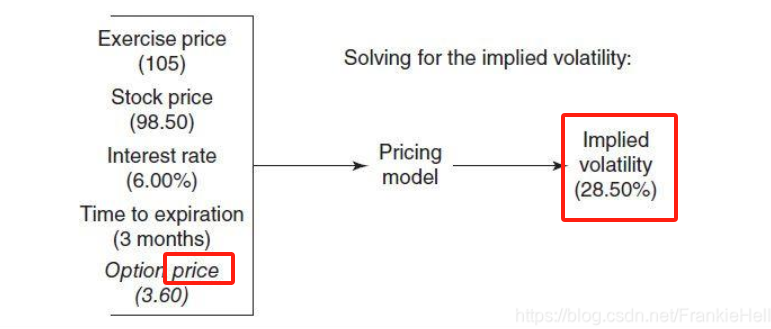

Solomon observes that the market price of the

put option in Exhibit 2 is $7.20. Lee responds that she used the historical

volatility of the GPX of 24% as an

input to the BSM model, and she explains the implications for the implied volatility

for the GPX.

Based

on Solomon’s observation about the model price and market price for the put

option in Exhibit 2, the implied volatility for the GPX is most likely:

选项:

A.less than the historical volatility.

equal to the historical volatility.

greater than the historical volatility.

解释:

The put is priced at $7.4890 by the BSM model

when using the historical volatility input of 24%. The market price is $7.20.

The BSM model overpricing suggests the implied volatility of the put must be lower

than 24%.

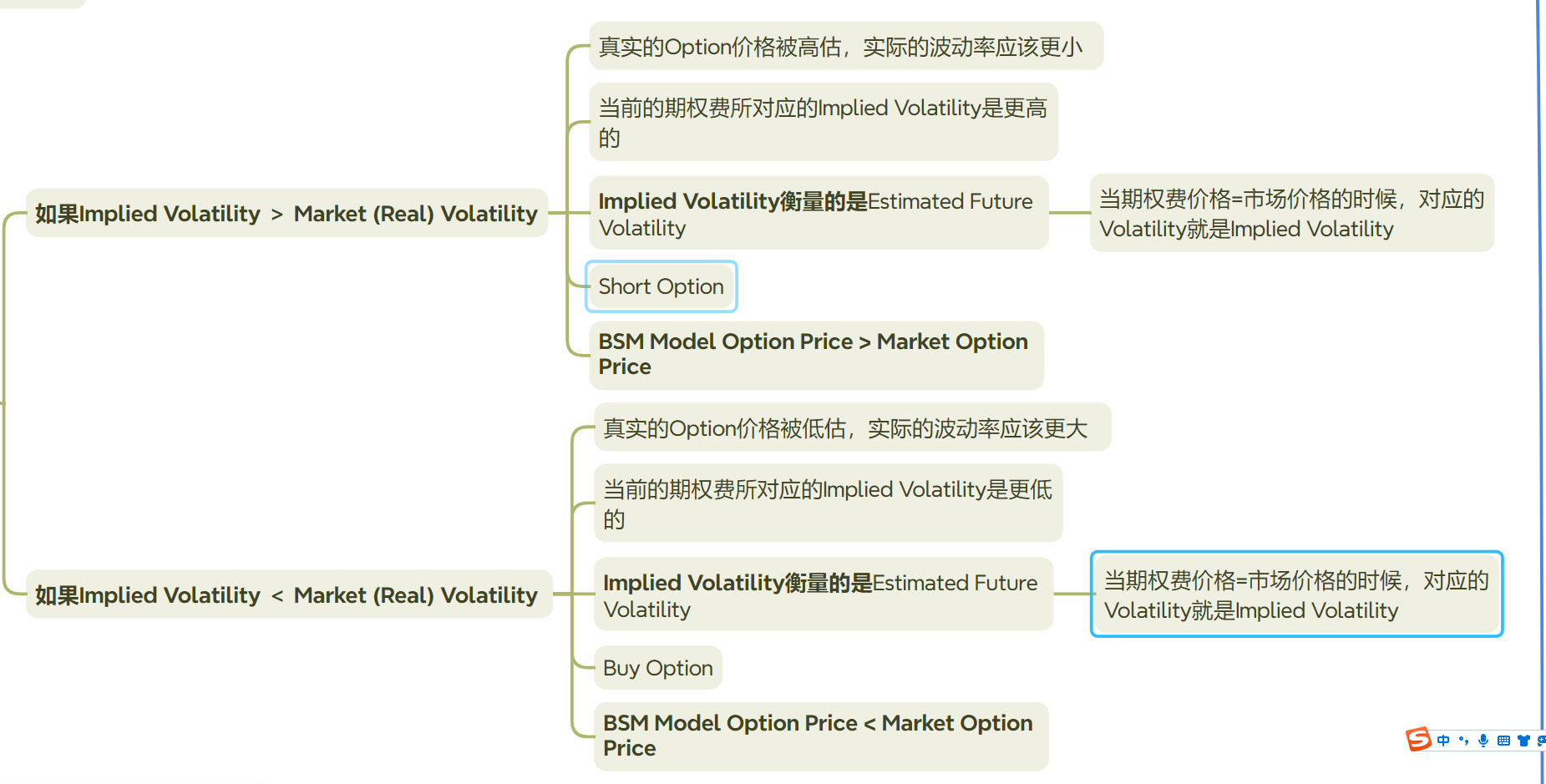

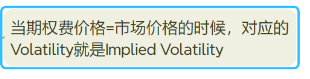

我看其他回答说Implied Volatility就是用当前市场的Option Value计算得出的,也就是7.2对应的volatility,但是老师强化课又用Implied Volatility和Market Volatility去做了对比判断高低估,我有点懵,老师可以解释一下吗?谢谢

另外可以麻烦老师看一下我这个图,能帮我看一下我理解的是否正确?里面有些错的地方吗?