NO.PZ202208300200000104

问题如下:

Assuming a 5% level of significance, the most appropriate conclusion that can be drawn from the Dickey–Fuller results reported in Exhibit 2 is that the:

选项:

A.test for a unit root is inconclusive for the dependent variable.

B.dependent variable exhibits a unit root but the independent variables do not.

C.independent variables exhibit unit roots but the dependent variable does not.

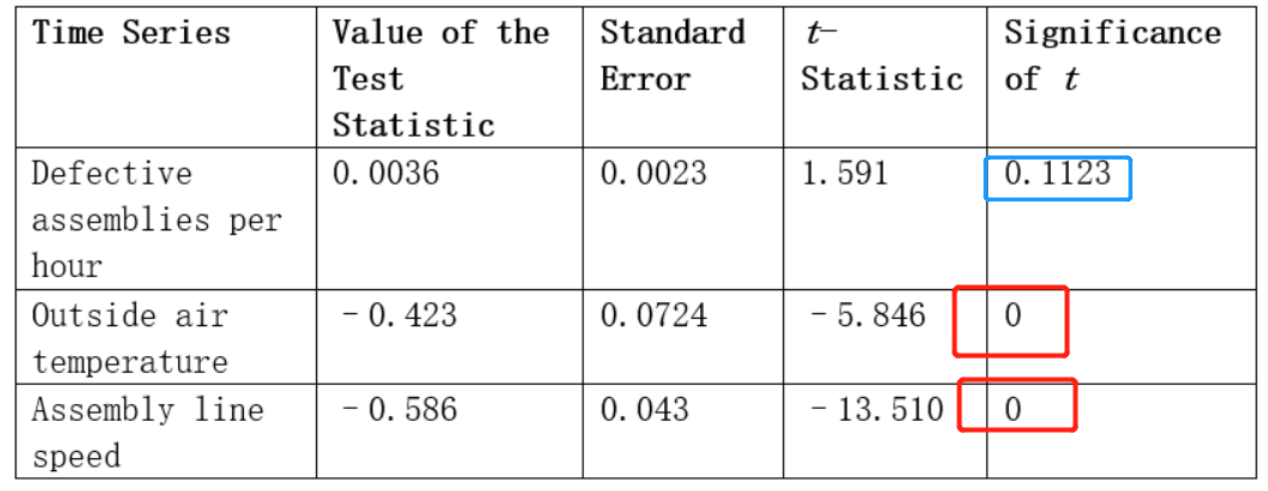

解释:

The Dickey–Fuller test uses a regression of the type:xt-xt-1 =b0+g xt-1+εt

The null hypothesis is H0: g= 0 versus the alternative hypothesis H1: g< 0 (a one-tail test). If g=0 the time series has a unit root and is nonstationary. Thus, if we fail to reject the null hypothesis, we accept the possibility that the time series has a unit root and is nonstationary. Based on the t ratios and their significance levels in Exhibit 2, we reject the null hypothesis that the coefficient is zero for both outside air temperature and assembly line speed (i.e., the independent variables). We do not reject the null for the dependent variable, defective assemblies per hour.

表格中的数字怎么和题目对应起来?完全不知道怎么用