NO.PZ2023090201000078

问题如下:

For a fixed-rate bond, when interest rates decrease, the future value of reinvested coupon payments most likely:

选项:

A.decreases and the market price of the bond increases. B.increases and the market price of the bond decreases. C.increases and the market price of the bond increases.解释:

A is correct.

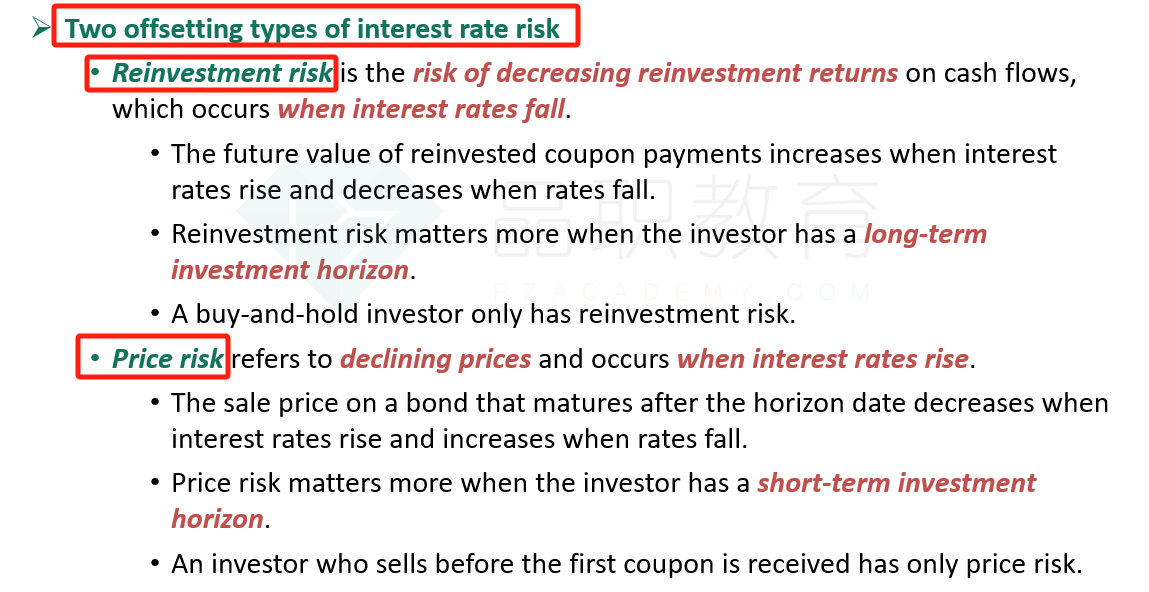

There are two offsetting types of interest rate risk that affect the bond investor: coupon reinvestment risk and market price risk. The future value of reinvested coupon payments (and in a portfolio, the principal on bonds that mature before the horizon date) increases when interest rates go up and decreases when rates go down. The sale price on a bond that matures after the horizon date (and thus needs to be sold) decreases when interest rates go up and increases when rates go down

考点:Reinvestment Risk & Price Risk

解析:当利率下降的时候,再投资收益会下降,债券价格会上升。市场利率的改变对再投资收益和债券价格的影响是呈反向关系的。

For a fixed-rate bond, when interest rates decrease, the future value of reinvested coupon payments most likely: