NO.PZ2023091701000087

问题如下:

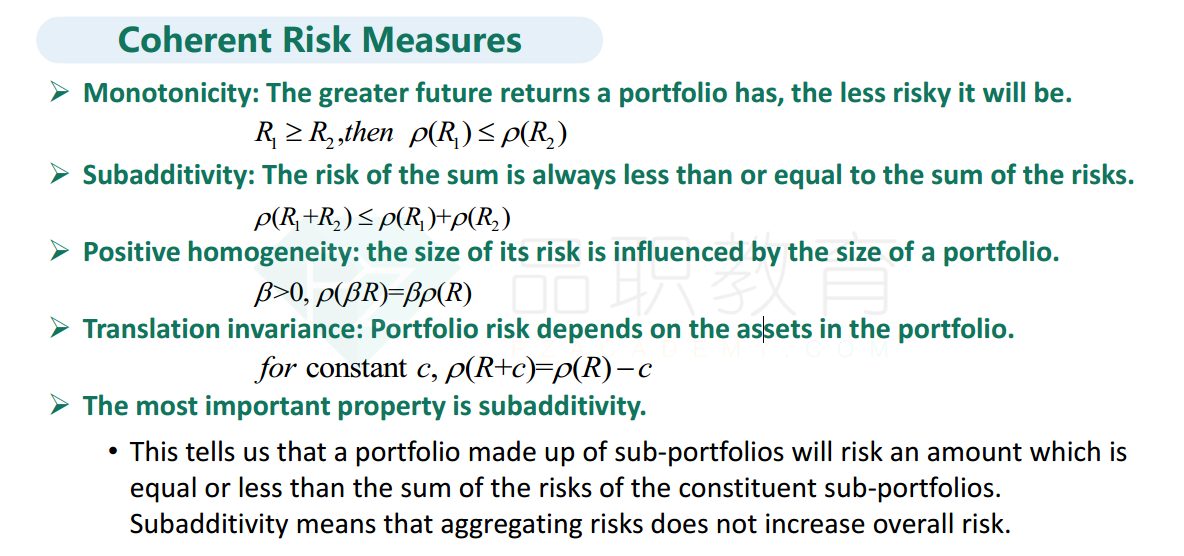

The CRO of a major bank is reviewing a new risk measure, W, with the risk team. The CRO runs a test on the new risk measure to determine if the measure is coherent and satisfies the property of translation invariance. Which of the following tests would correctly determine that the risk measure W exhibits translation invariance?

选项:

A.When cash is added to a portfolio, the value of W for that portfolio should decrease by the amount of cash that is added.

B.When W is used to measure the risk of two portfolios A and B, then W(A) + W(B) should be less than or equal to W(A+B).

C.When W is used to measure the risk of two portfolios A and B, and if portfolio A always produces a worse outcome than portfolio B, then W(A) should always be higher than W(B).

D.When W is used to measure the risk of portfolio A, and if all exposures in portfolio A are increased by a constant factor, then W(A) should increase proportionally by that factor.

解释:

A is correct. According to the property of translation invariance, adding an amount of cash, K, into a portfolio will decrease the risk measure by K. Therefore, choice A correctly describes translation invariance.

B is incorrect. This is a test for subadditivity. According to the property of subadditivity, given two portfolios A and B, the risk measure for the portfolio formed by merging A and B will be less than or equal to the sum of the risk measures for A and B.

C is incorrect. This is a test for monotonicity. According to the property of monotonicity, a portfolio that produces consistently worse results in comparison to another portfolio will have a higher risk measure.

D is incorrect. This is a test of homogeneity. According to the property of homogeneity, changing the size of a portfolio by multiplying the amount of all components by λ results in the risk measure being multiplied by λ.

可以解释一下这个特性吗,理解的不是很充分