NO.PZ2023091802000092

问题如下:

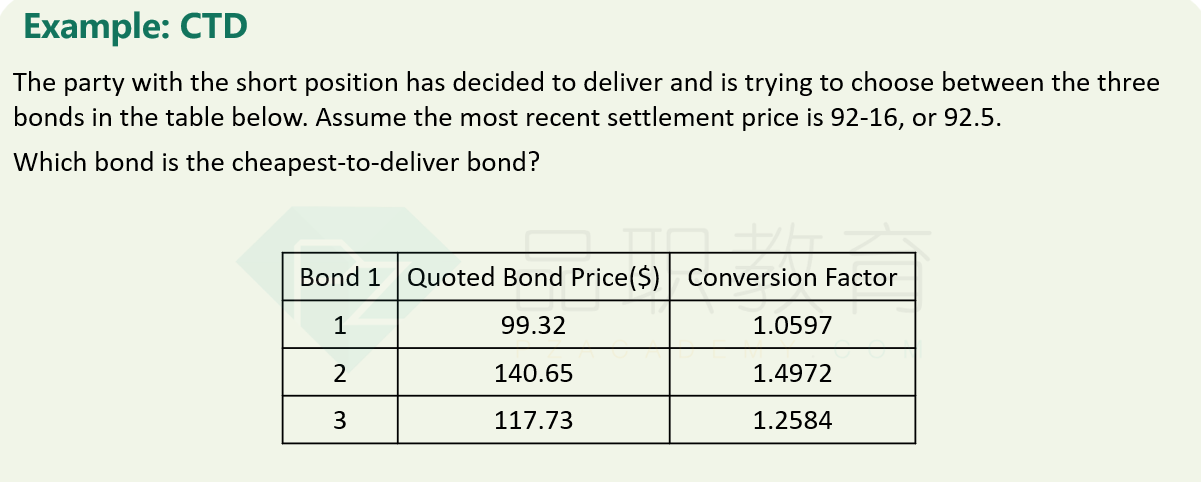

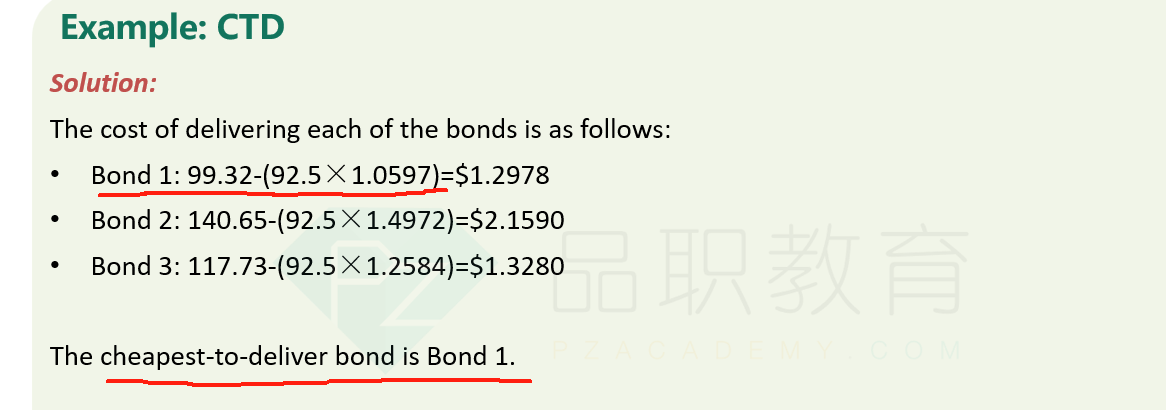

The owner of a

fixed-income portfolio worth USD 12 million that has duration of 4.0 seeks to

hedge the position with 3-month US Treasury futures, which are currently

trading at USD 101.25 per USD 100 face value. Given that each contract requires

the delivery of USD 100,000 face value worth of bonds, which of the following

qualifying bonds would be cheapest to deliver?

选项:

A.Bond A

B.Bond B

Bond C

Bond D

解释:

求这题的计算过程