NO.PZ2020021002000112

问题如下:

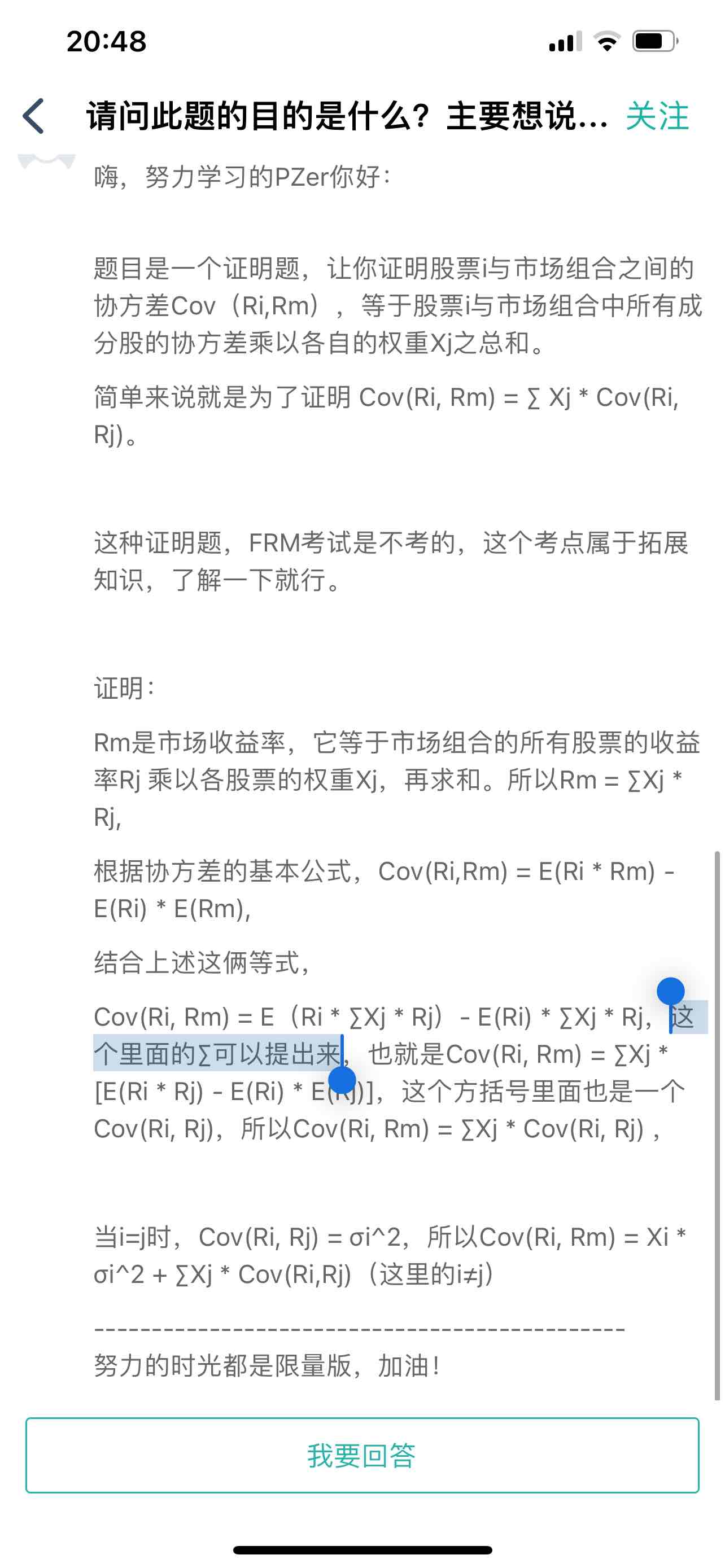

Prove that the covariance of stock i with the market portfolio is equal to the sum of the covariances of stock i with all the n stocks included in the market portfolio multiplied by the corresponding proportions xi.

解释:

老师,这里的这个里面的∑Xj为何可以提出来?∑Xj并不是一个常数啊,是X1+X2+…Xj