NO.PZ2023041003000044

问题如下:

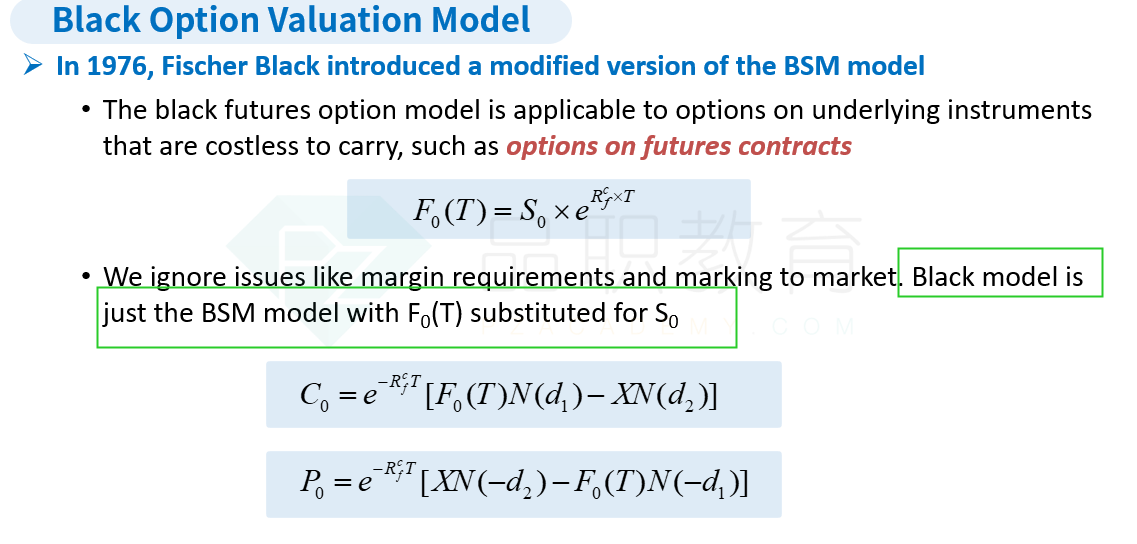

The Black model valuation and selected outputs

for options on another of Solomon’s holdings, the GPX 500 Index (GPX), are shown in

Exhibit 2. The spot index level for the GPX is 187.95, and the index is assumed

to pay a continuous dividend at a rate of 2.2% (5) over the life of the options

being valued, which expire in 0.36 years. A futures contract on the GPX also

expiring in 0.36 years is currently priced at 186.73.

What are the correct spot value (S) and the

risk-free rate (r) that Lee should use as inputs for the Black model?

选项:

A.186.73 and 0.39%, respectively

186.73 and 2.20%, respectively

187.95 and 2.20%, respectively

解释:

Black’s model to value a call option on a

futures contract is c = e-rT[F0(T)N(d1) - XN(d2)]. The underlying F0 is the futures price (186.73). The correct discount

rate is the risk-free rate, r = 0.39%.

是因为明确说了black model,所以只能用远期价格,而不能用现货价格187.95扣除连续分红,得到186.47吗?虽然选对了答案,后者算出186.47作为bsm输入变量的逻辑正确吗?