NO.PZ2022123001000051

问题如下:

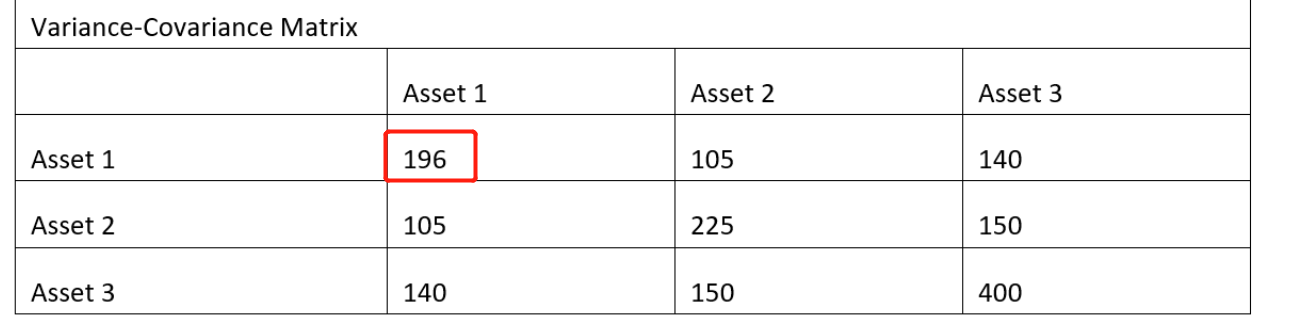

Lena Hunziger has designed the three-asset portfolio summarized below:

Hunziger estimated the portfolio return to be 6.3%. What is the portfolio standard deviation?

选项:

A.13.07%

B.13.88%

C.14.62%

解释:

For a three-asset portfolio, the portfolio variance is

为什么这两相乘等于196