NO.PZ2021061002000065

问题如下:

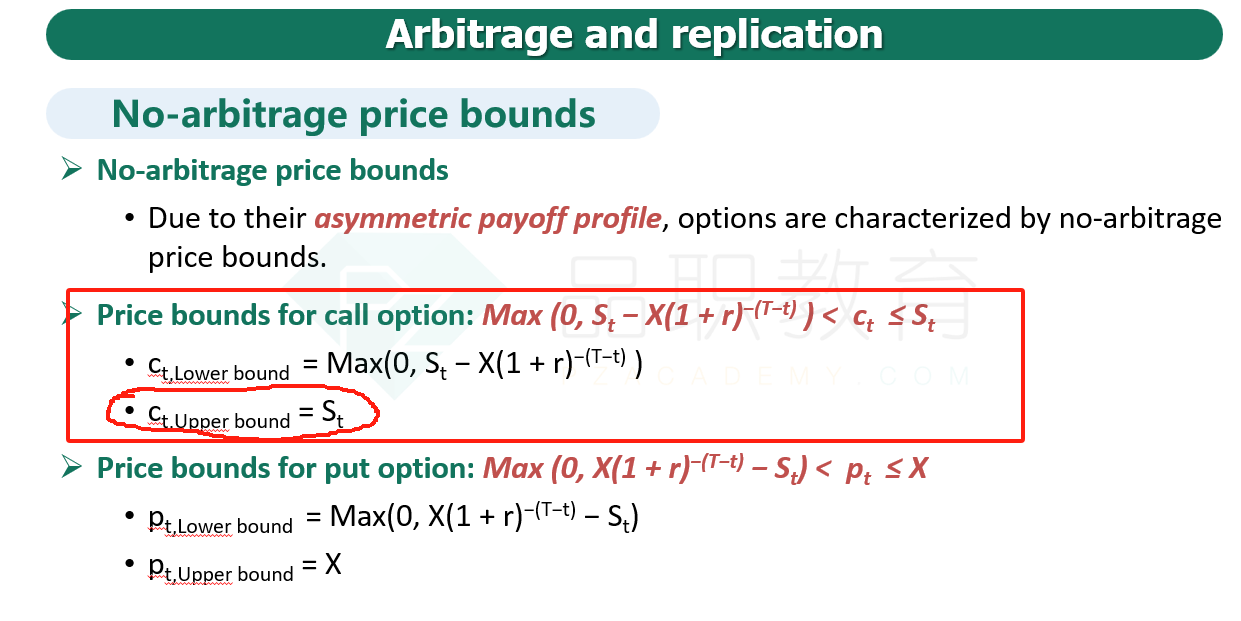

Suppose the strike price of a one-year call option is CAD100, the risk free rate is 2%. At time 0, the underlying asset, S0, trades at CAD98, now six months have passed, the underlying asset, St, trades at CAD102.

选项:

A.

The upper bound of the call option is CAD102;

the lower bound of the call option is 0;

B.

The upper bound of the call option is CAD102;

the lower bound of the call option is CAD2.9852;

C.

The upper bound of the call option is CAD2.9852; the lower bound of the call option is 0;

解释:

中文解析:

计算如下:

ct,Lower bound = Max(0, St − X(1 + r)−(T−t) ) = Max (0, 102 – 100(1+2%)-0.5)

= CAD2.9852

ct,Upper bound = St = CAD102

不是S-X和0之间的取最大值么,102怎么得到的