问题如下图:

选项:

A.

B.

C.

解释:

老师您好,这道题目考查的知识点是哪个呢?谢谢解答🙏

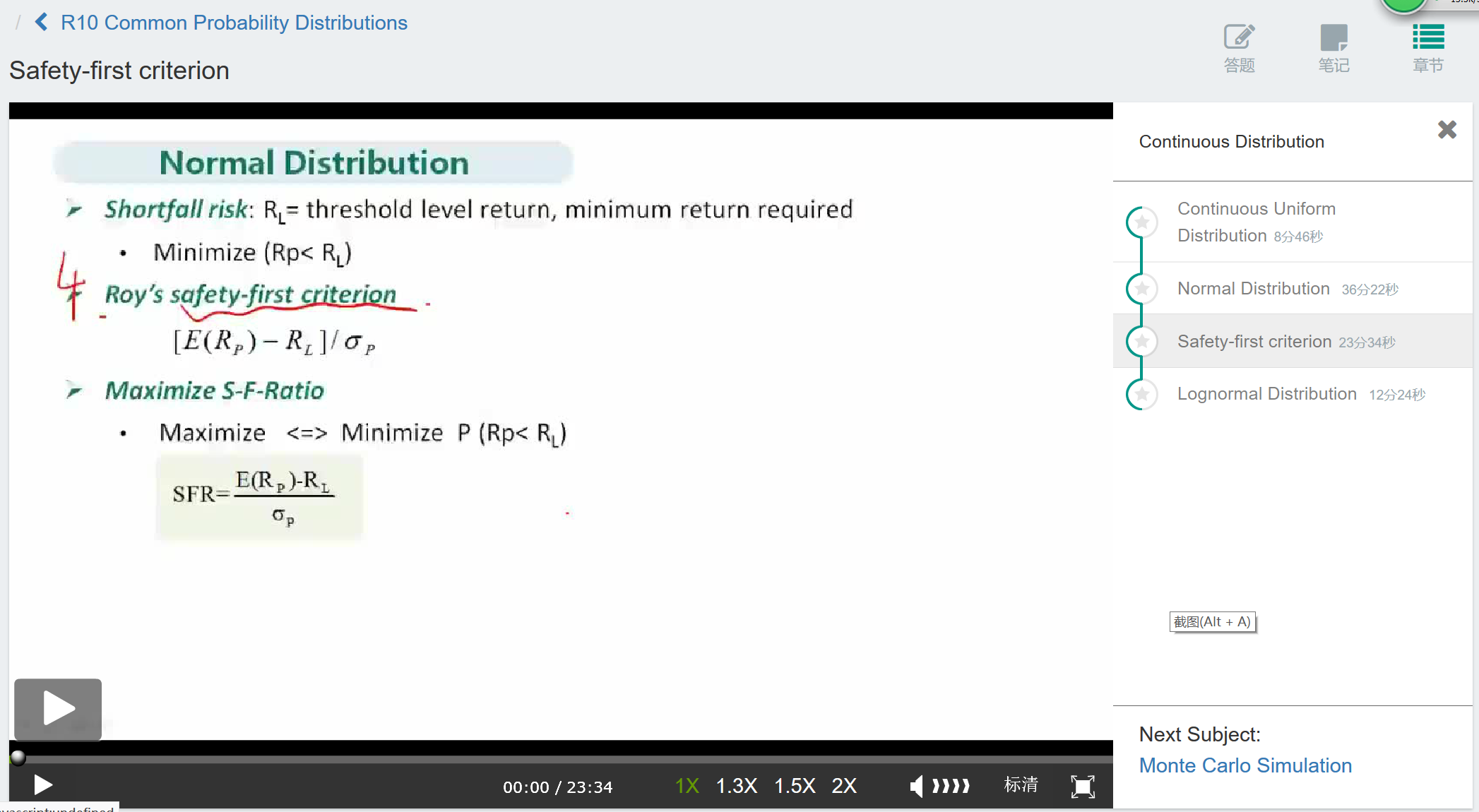

NO.PZ2017092702000101 问题如下 A client holng a £2,000,000 portfolio wants to with£90,000 in one yewithout invang the principal. Accorng to Roy’s safety-first criterion, whiof the following portfolio allocations is optimal? A.Allocation B.Allocation C.Allocation B is correct. Allocation B hthe highest safety-first ratio. The thresholreturn level RL for the portfolio is £90,000/£2,000,000 = 4.5%, thus any return less thRL = 4.5% will inva the portfolio principal. To compute the allocation this safety-first optimal, selethe alternative with the highest ratio:lE[(Rp−RL)]σPAllocation A =6.5−4.58.35=0.240Allocation B =7.5−4.510.21=0.294Allocation C =8.5−4.514.34=0.279{l}\frac{E{\lbrack{(R_p-R_L)}\rbrack}}{\sigma_P}\\Allocation\text{ }A\text{ =}\frac{6.5-4.5}{8.35}=0.240\\Allocation\text{ }B\text{ =}\frac{7.5-4.5}{10.21}=0.294\\Allocation\text{ }C\text{ =}\frac{8.5-4.5}{14.34}=0.279lσPE[(Rp−RL)]Allocation A =8.356.5−4.5=0.240Allocation B =10.217.5−4.5=0.294Allocation C =14.348.5−4.5=0.279 1

NO.PZ2017092702000101问题如下 A client holng a £2,000,000 portfolio wants to with£90,000 in one yewithout invang the principal. Accorng to Roy’s safety-first criterion, whiof the following portfolio allocations is optimal?A.Allocation A B.Allocation BC.Allocation CB is correct. Allocation B hthe highest safety-first ratio. The thresholreturn level RL for the portfolio is £90,000/£2,000,000 = 4.5%, thus any return less thRL = 4.5% will inva the portfolio principal. To compute the allocation this safety-first optimal, selethe alternative with the highest ratio:lE[(Rp−RL)]σPAllocation A =6.5−4.58.35=0.240Allocation B =7.5−4.510.21=0.294Allocation C =8.5−4.514.34=0.279{l}\frac{E{\lbrack{(R_p-R_L)}\rbrack}}{\sigma_P}\\Allocation\text{ }A\text{ =}\frac{6.5-4.5}{8.35}=0.240\\Allocation\text{ }B\text{ =}\frac{7.5-4.5}{10.21}=0.294\\Allocation\text{ }C\text{ =}\frac{8.5-4.5}{14.34}=0.279lσPE[(Rp−RL)]Allocation A =8.356.5−4.5=0.240Allocation B =10.217.5−4.5=0.294Allocation C =14.348.5−4.5=0.279 如题,公式看起来一样呀。视频里没有讲

NO.PZ2017092702000101问题如下A client holng a £2,000,000 portfolio wants to with£90,000 in one yewithout invang the principal. Accorng to Roy’s safety-first criterion, whiof the following portfolio allocations is optimal?A.Allocation A B.Allocation BC.Allocation CB is correct. Allocation B hthe highest safety-first ratio. The thresholreturn level RL for the portfolio is £90,000/£2,000,000 = 4.5%, thus any return less thRL = 4.5% will inva the portfolio principal. To compute the allocation this safety-first optimal, selethe alternative with the highest ratio:lE[(Rp−RL)]σPAllocation A =6.5−4.58.35=0.240Allocation B =7.5−4.510.21=0.294Allocation C =8.5−4.514.34=0.279{l}\frac{E{\lbrack{(R_p-R_L)}\rbrack}}{\sigma_P}\\Allocation\text{ }A\text{ =}\frac{6.5-4.5}{8.35}=0.240\\Allocation\text{ }B\text{ =}\frac{7.5-4.5}{10.21}=0.294\\Allocation\text{ }C\text{ =}\frac{8.5-4.5}{14.34}=0.279lσPE[(Rp−RL)]Allocation A =8.356.5−4.5=0.240Allocation B =10.217.5−4.5=0.294Allocation C =14.348.5−4.5=0.279 我是2022年11月份的考生,想请问在听课时没有听到罗伊第一安全比率这个知识点,强化串讲也没有,是被取消了么

NO.PZ2017092702000101 Allocation B Allocation C B is correct. Allocation B hthe highest safety-first ratio. The thresholreturn level RL for the portfolio is £90,000/£2,000,000 = 4.5%, thus any return less thRL = 4.5% will inva the portfolio principal. To compute the allocation this safety-first optimal, selethe alternative with the highest ratio: lE[(Rp−RL)]σPAllocation A =6.5−4.58.35=0.240Allocation B =7.5−4.510.21=0.294Allocation C =8.5−4.514.34=0.279{l}\frac{E{\lbrack{(R_p-R_L)}\rbrack}}{\sigma_P}\\Allocation\text{ }A\text{ =}\frac{6.5-4.5}{8.35}=0.240\\Allocation\text{ }B\text{ =}\frac{7.5-4.5}{10.21}=0.294\\Allocation\text{ }C\text{ =}\frac{8.5-4.5}{14.34}=0.279lσPE[(Rp−RL)]Allocation A =8.356.5−4.5=0.240Allocation B =10.217.5−4.5=0.294Allocation C =14.348.5−4.5=0.279 如标题、为什么选最大的那个、不太懂

Allocation B Allocation C B is correct. Allocation B hthe highest safety-first ratio. The thresholreturn level RL for the portfolio is £90,000/£2,000,000 = 4.5%, thus any return less thRL = 4.5% will inva the portfolio principal. To compute the allocation this safety-first optimal, selethe alternative with the highest ratio: lE[(Rp−RL)]σPAllocation A =6.5−4.58.35=0.240Allocation B =7.5−4.510.21=0.294Allocation C =8.5−4.514.34=0.279{l}\frac{E{\lbrack{(R_p-R_L)}\rbrack}}{\sigma_P}\\Allocation\text{ }A\text{ =}\frac{6.5-4.5}{8.35}=0.240\\Allocation\text{ }B\text{ =}\frac{7.5-4.5}{10.21}=0.294\\Allocation\text{ }C\text{ =}\frac{8.5-4.5}{14.34}=0.279lσPE[(Rp−RL)]Allocation A =8.356.5−4.5=0.240Allocation B =10.217.5−4.5=0.294Allocation C =14.348.5−4.5=0.279 为什么RL是用9000/20000呢?