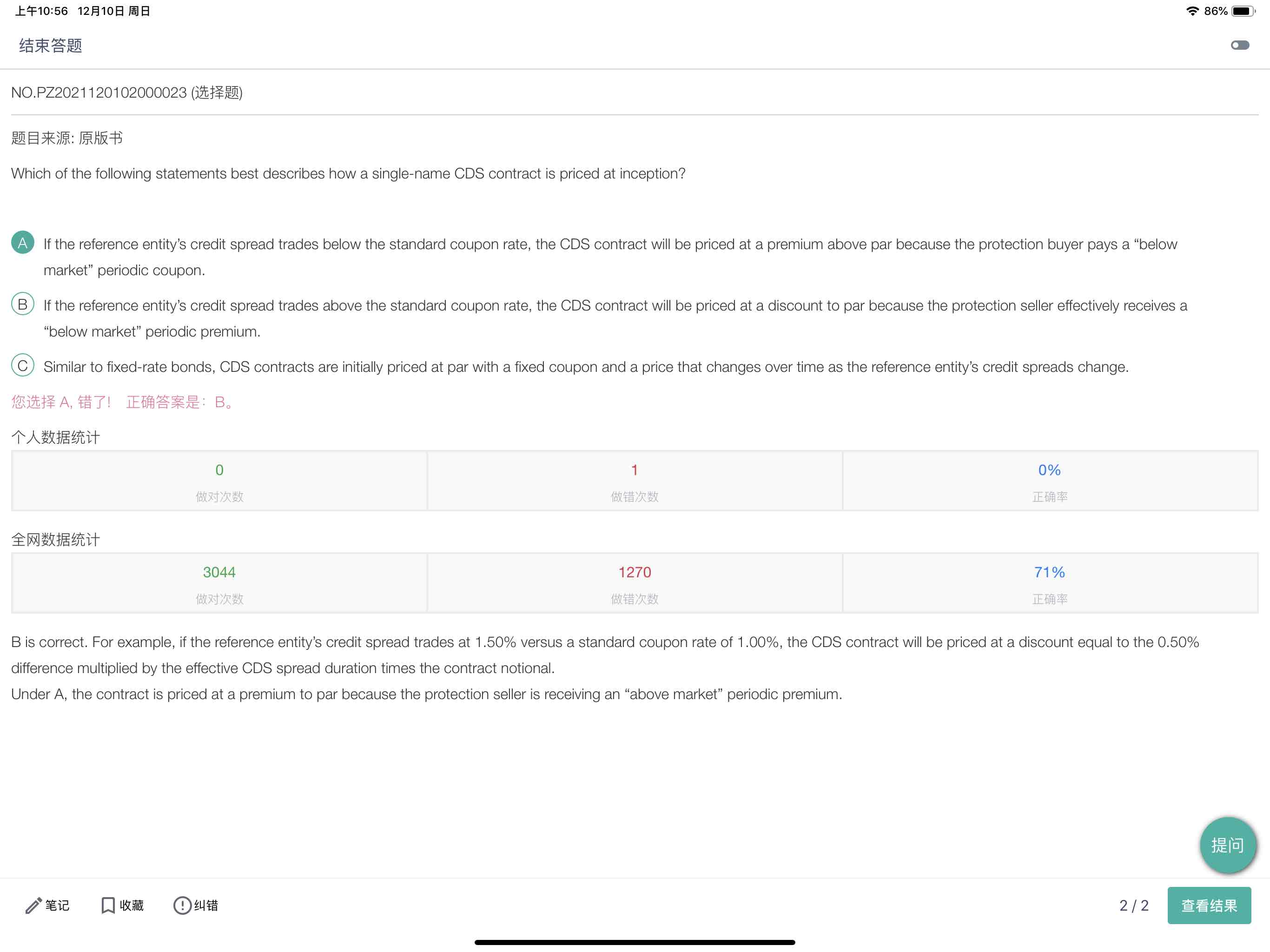

A选项为什么错误呢?,B选项中的seller receive below market premium 又应该怎么解释?如果 spread比coupon大的话,那么不是应该buyer受益吗

pzqa31 · 2023年12月11日

嗨,努力学习的PZer你好:

CDS price=1+(fixed coupon-spread)*ED

如果期初fixed coupon>spread,则CDS price>1,溢价发行

如果期初fixed coupon<spread,则CDS price<1,折价发行

A选项:这里的market指的是与当前reference风险状况相对应的periodic fixed coupon水平,而不是标准化的fixed coupon(1%或者5%)。

比如,credit spread<fixed coupon,说明当前标准化的fixed coupon(1%或者5%)定高了,它是above market periodic coupon,应该支付或者收到低于标准化的fixed coupon(1%或者5%)的periodic coupon,答案解析关于A说的也不对哈,正确的表述是:If the reference entity’s credit spread trades below the standard coupon rate, the CDS contract will be priced at a premium above par because the protection buyer pays a “above market” periodic coupon.

反之,如果credit spread>fixed coupon,说明支付的fixed coupon少了,应该支付更多periodic coupon,如果进入这份合约,seller收到periodic coupon是below market的。

----------------------------------------------加油吧,让我们一起遇见更好的自己!