NO.PZ202305230100004904

问题如下:

If the yields-to-maturity for all three bonds were to increase by 100 bps, which bond has the greatest anticipated decrease in price?

选项:

A.Bond One

Bond Two

Bond Three

解释:

B is correct.

能解释下这道题吗,modified duration 什么意思

pzqa015 · 2023年11月18日

嗨,努力学习的PZer你好:

modified duration是利率变动△y,债券价格的变动幅度。△P/P=-modified duration*△y,如果利率上涨相同幅度,modified duration大的,债券收益率下的多,money duration=modified duration*MV,如果利率上涨相同幅度,money duration大的,债券value下降的最多,这道题问的是great decrease in price,选择债券value下降最多的,所以,应该计算money duration,选择money duration最大的。

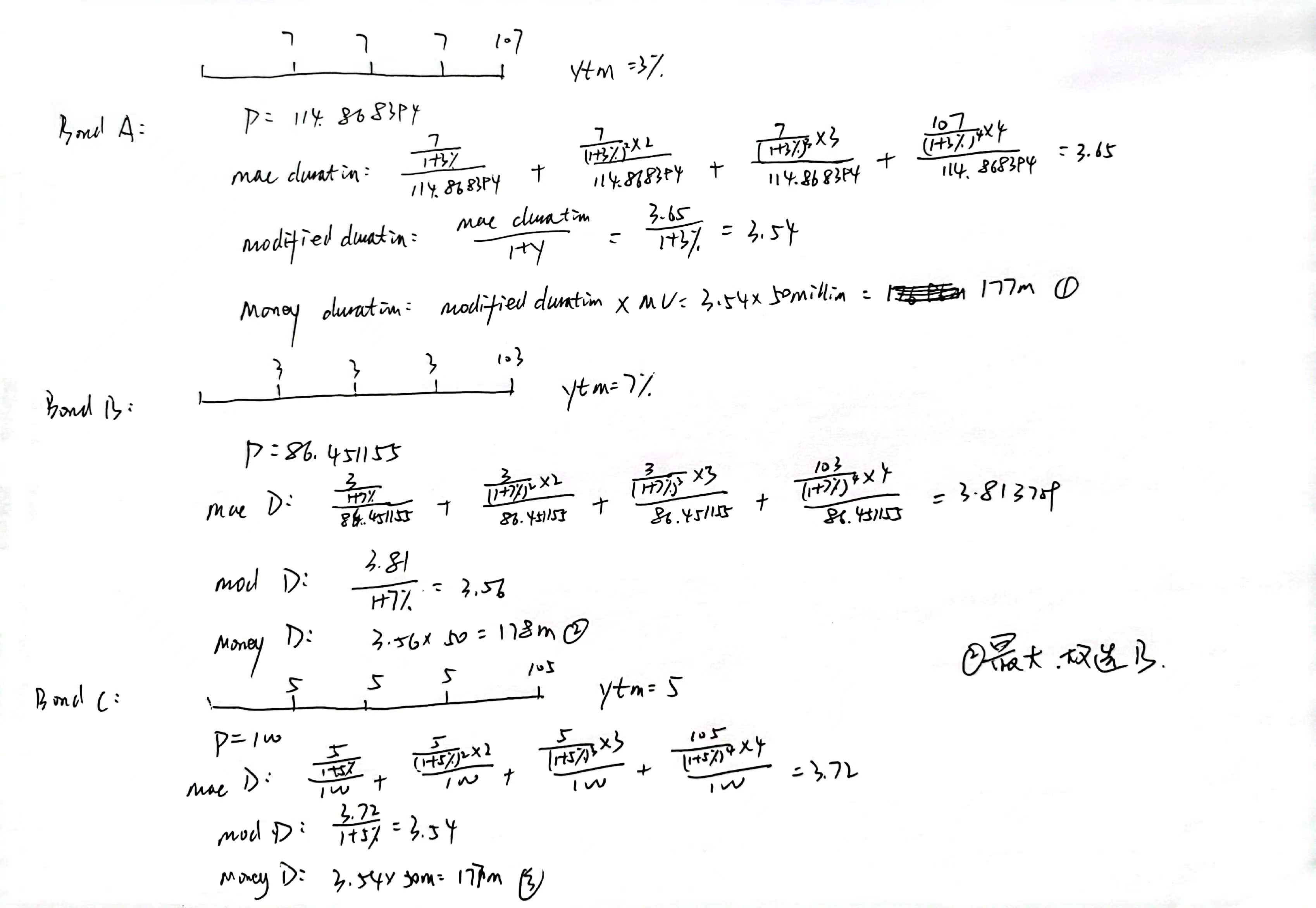

解析里面的计算不准确,以下图为准吧

----------------------------------------------

就算太阳没有迎着我们而来,我们正在朝着它而去,加油!

Chinazdk · 2024年02月13日

一共要分8期 半年付息

NO.PZ202305230100004904 问题如下 If the yiel-to-maturity for all three bon were to increase 100 bps, whibonhthe greatest anticipatecrease in price? A.BonOne B.BonTwo C.BonThree B is correct. 价格与收益率曲线有涨多跌少的特性,三只债券的收益率不同,对应相同收益率波动幅度不同,收益率低的价格波动大

NO.PZ202305230100004904问题如下 If the yiel-to-maturity for all three bon were to increase 100 bps, whibonhthe greatest anticipatecrease in price? A.BonOneB.BonTwoC.BonThree B is correct. 解析money ration为何用mofie以 50?

NO.PZ202305230100004904 问题如下 If the yiel-to-maturity for all three bon were to increase 100 bps, whibonhthe greatest anticipatecrease in price? A.BonOne B.BonTwo C.BonThree B is correct. 能下这道题及知识点吗

NO.PZ202305230100004904问题如下 If the yiel-to-maturity for all three bon were to increase 100 bps, whibonhthe greatest anticipatecrease in price? A.BonOneB.BonTwoC.BonThree B is correct. 最后一行change in value怎么计算?