NO.PZ202207040100000403

问题如下:

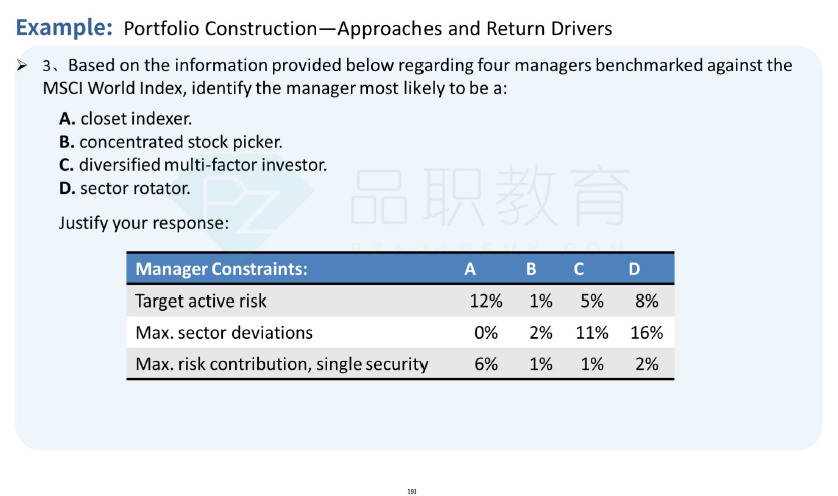

Among the funds shown in Exhibit 2, which one is most likely managed using a diversified multi-factor investor approach?

选项:

A.Fund X

B.Fund Y

C.Fund Z

解释:

SolutionC is correct. The risk targets for Fund Z are most likely those of a manager using a diversified multi-factor approach. Low single-security risk of 1% and modest overall portfolio risk of 4%, combined with flexibility on sector risk, demonstrate a highly diversified portfolio that primarily emphasizes factor exposures. Fund X has risk targets consistent with an emphasis on stock picking—namely, high active risk, high exposure to risk from a single security, and low sector deviations. Fund Y has risk targets consistent with an emphasis on sector rotation—namely, high active risk and a high tolerance for sector deviations.

A is incorrect. Fund X has risk targets consistent with an emphasis on stock picking—namely, high active risk, high exposure to risk from a single security, and low sector deviations.

B is incorrect. Fund Y has risk targets consistent with an emphasis on sector rotation—namely, high active risk and a high tolerance for sector deviations.

请老师解释一下表格里的几个名词的意思和作用