NO.PZ2023091802000096

问题如下:

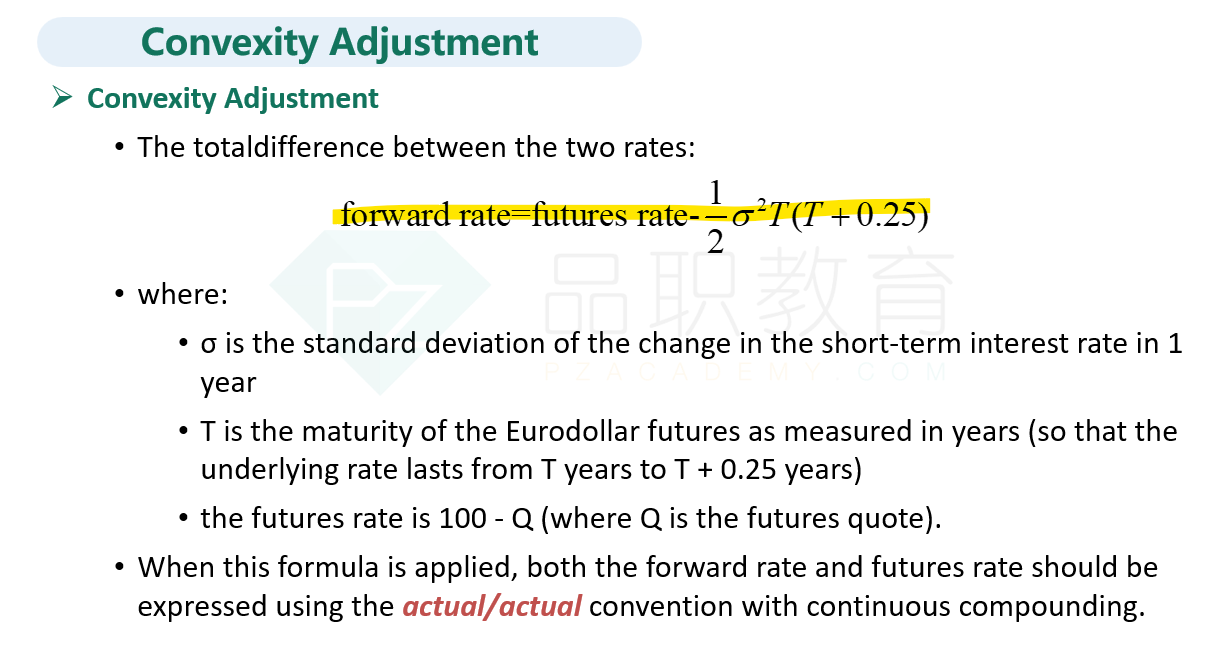

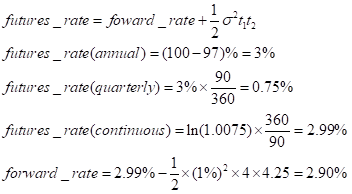

The four-year Eurodollar futures quote is 97.00. The volatility of the short-term interest rate (LIBOR) is 1.0%, expressed with continuous compounding. What is the equivalent forward rate, adjusted for convexity, given in ACT/360 day count with continuous compounding (i.e., the Eurodollar futures contract gives LIBOR in quarterly compounding ACT/360, so convert to continuous but a day count conversion is not needed)?

选项:

A.2.90%

B.2.95%

C.2.99%

D.3.00%

解释:

如题