NO.PZ2023091802000042

问题如下:

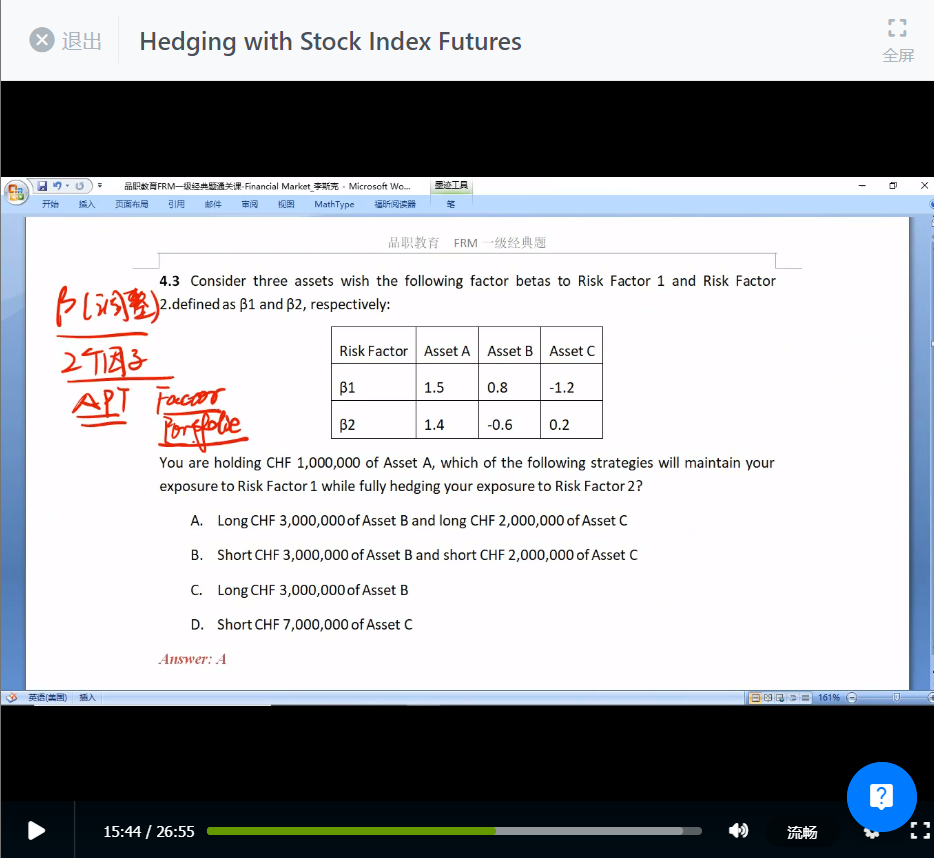

Consider three assets wish the following factor betas to Risk Factor

1 and Risk Factor 2.defined as β1 and β2, respectively:

You are holding CHF 1,000,000 of Asset A, which of the following strategies will maintain your exposure to Risk Factor 1 while fully hedging your exposure to Risk Factor 2?

选项:

A.

Long CHF 3,000,000 of Asset B and long CHF 2,000,000 of Asset C

B.

Short CHF 3,000,000 of Asset B and short CHF 2,000,000 of Asset C

C.

Long CHF 3,000,000 of Asset B

D.

Short CHF 7,000,000 of Asset C

解释:

看到这题只想到带公式,但是发现好像缺少一些条件,然后就不知道怎么做了