NO.PZ2023010301000041

问题如下:

An inverse floater will most likely have:

选项:

A.a maximum coupon rate.

a face value that changes as the reference rate changes.

a coupon rate that changes by more than the change in the reference rate.

解释:

Correct Answer: A

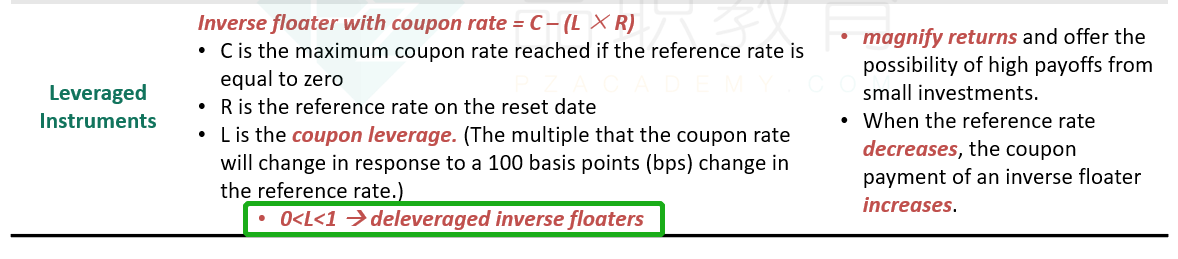

The general formula for the coupon rate of an inverse floater is C – (L × R), where C is the maximum coupon rate if the reference rate (R) is equal to zero and L is the coupon leverage, which is greater than zero.

B is incorrect. The face value of an inverse floater does not change as the reference rate changes; rather, the coupon rate changes.

C is incorrect. Inverse floaters can have leverage less than 1 (deleveraged inverse floaters), so the coupon rate changes by less than the change in the reference rate; leverage greater than 1 (leveraged inverse floaters), so the coupon rate changes by more than the change in the reference rate; or leverage equal to 1, so the coupon rate changes by the same amount as the change in the reference rate.

没看明白,选项和问题。