NO.PZ2023040502000009

问题如下:

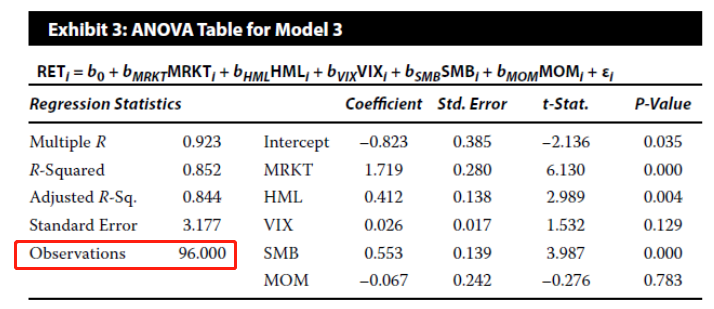

You are a junior analyst at an asset management firm. Your supervisor asks you to analyze the return drivers for one of the firm’s portfolios. She asks you to construct a regression model of the portfolio’s monthly excess returns (RET) against three factors: the market excess return (MRKT), a value factor (HML), and the monthly percentage change in a volatility index (VIX). You collect the data and run the regression. After completing the first regression (Model 1), you review the ANOVA results with your supervisor.

Model 1: RETi = b0 + bMRKTMRKTi

+ bHMLHMLi + bVIXVIXi + εi.

Model 2: RETi = b0 + bMRKTMRKTi

+ bHMLHMLi + bVIXVIXi + bSMBSMBi

+ εi.

Model 3: RETi = b0 + bMRKTMRKTi

+ bHMLHMLi + bVIXVIXi + bSMBSMBi

+ bMOMMOMi + εi.

The regression statistics and ANOVA results for the

Model 1 and Model 3 are shown in Exhibit 1 and Exhibit 3

Calculate the joint F-statistic and determine whether

SMB and MOM together contribute to explaining RET in Model 3 at a 1%

significance level (use a critical value of 4.849).

选项:

A.2.216, so SMB and MOM together do not contribute to

explaining RET

8.863, so SMB and MOM together do contribute to

explaining RET

9.454, so SMB and MOM together do contribute to

explaining RET

解释:

B is correct. To determine whether SMB and MOM

together contribute to the explanation of RET, at least one of the coefficients

must be non-zero. So, H0:bSMB = bMOM = 0 and Ha: bSMB

≠ 0 and/or bMOM ≠ 0.

We use the F-statistic, where

,

,

with q = 2 and n – k – 1 = 90 degrees of

freedom. The test is one-tailed, right side, with α = 1%, so the critical

F-value is 4.849.

Model 1 does not include SMB and MOM, so it is

the restricted model. Model3 includes all of the variables of Model 1 as well

as SMB and MOM, so it is the unrestricted model.

Using data in Exhibit 1 and Exhibit 3, the joint

F-statistic is calculated as

.

.

Since 8.863 > 4.849, we

reject H0. Thus, SMB and MOM together do contribute to the

explanation of RET in Model 3 at a 1% significance level.

老师,您好!

本题的F统计量中的n-k-1 = 95-5-1 = 89,应该是89吧?怎么是90呢? 另外,the critical F-value is 4.849.是怎么得到的呢?谢谢!