NO.PZ2022123001000133

问题如下:

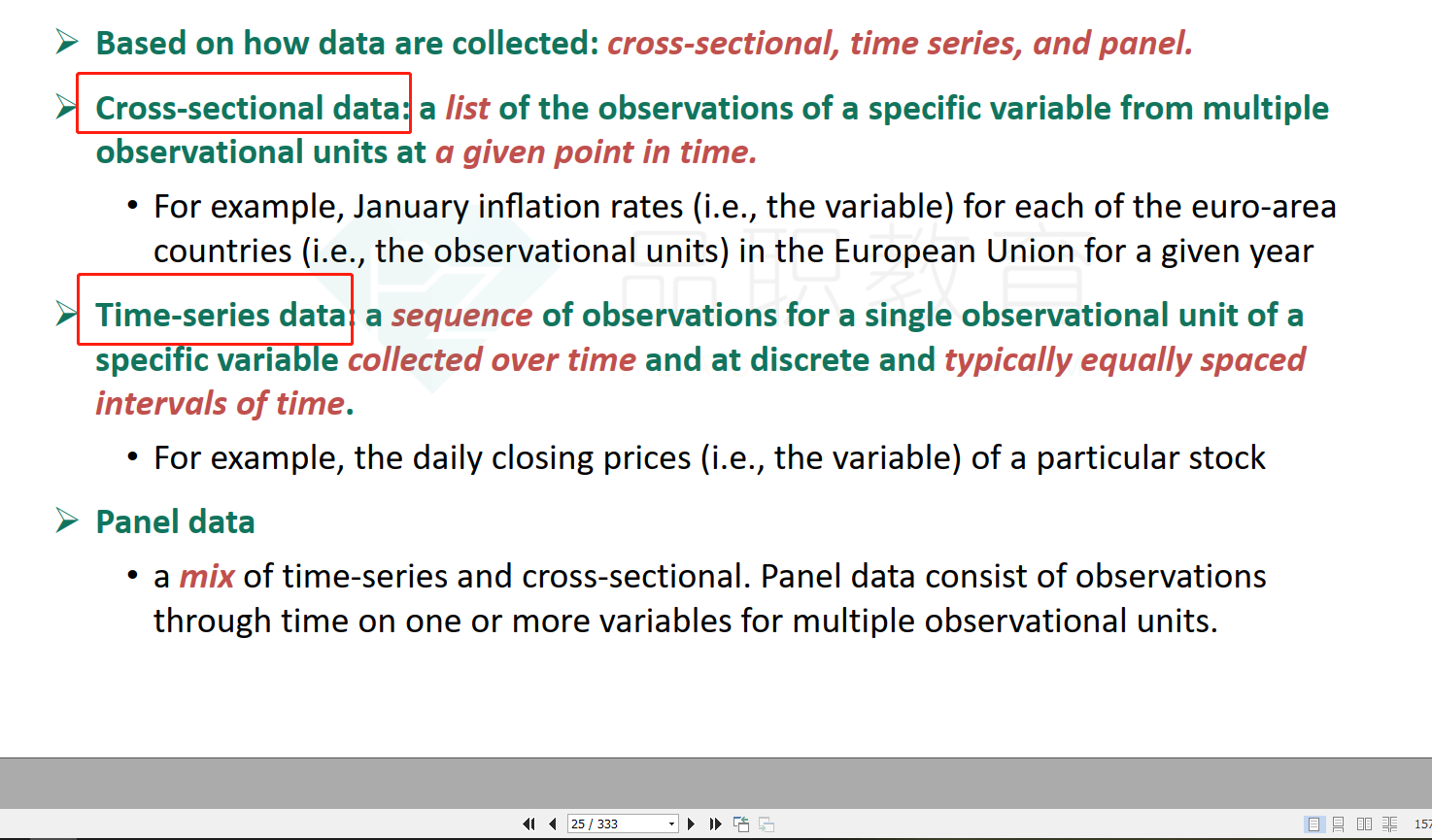

Jill Batten wants to study the relationships between Stellar monthly common stock returns and the previous month’s percentage change in the US Consumer Price Index for Energy (CPIENG). He runs a regression analysis using Stellar monthly returns as the dependent variable and the monthly change in CPIENG as the independent variable. Which of the following best describes Batten’s regression?

选项:

A.Time-series regression B.Cross-sectional regression C.Time-series and cross-sectional regression解释:

The data are observations over time.

用的是两家公司的不同时间的数据 为什么不也是cross-sectional呢