NO.PZ201812100100000502 问题如下 Baseon Exhibits 1 an2, the translation austment for TriofinB’s liabilities into Triofins presentation currenfor the six months en31 cember 2016 is: A.negative. B.zero. C.positive. C is correct.The monetary balansheet items for TriofinB are translatethe current exchange rate, whireflects ththe Borlianllweakenering the periorelative to the Norvolt euro. The rate of 30 June 2016 wBR.15/NER (or NER0.8696/BR anof 31 cember 2016 wBR.20/NER (or NER0.8333/BR. Therefore, notes payable translates to NER416,667 (BR00,000 × NER/BR.8333) of 31 cember 2016, comparewith NER434,783 (BR00,000 × NER/BR.8696) of 30 June 2016. Thus, the translation austment for liabilities is positive.考点tempormetholiability转换解析tempormethomonetary asset/liability转换使用current exchange rate,这道题问的是translation austment,其实就是问的是这6个月期间,期初转换完的liability和期末转换完的liability的变化量。6个月期间的汇率有变化,所以6个月之前转换的liability金额跟6个月之后的金额肯定不同,这个差额就是translation austment。子公司B的负债转换成NER,六个月前后的汇率分别为1.15BRNER和1.20BRNER子公司B的负债只有notes payable一项,转换为NER2016年6月30日是500,000/1.15=434,783, 2016年12月31日是500,000/1.2=416,667。转换后的金额变小了,是positive austment。 老师,我这里应该是把一些概念搞混了。隐约记得 何老师讲过 translation a.不是特指current metho计入B/S得调整吗, 然后tempormetho在P L下调整 translation g/l? 所以我看到题目已知是tempormetho就选了zero。记错的部分请老师指正谢谢

2023-04-24 23:14

1 · 回答

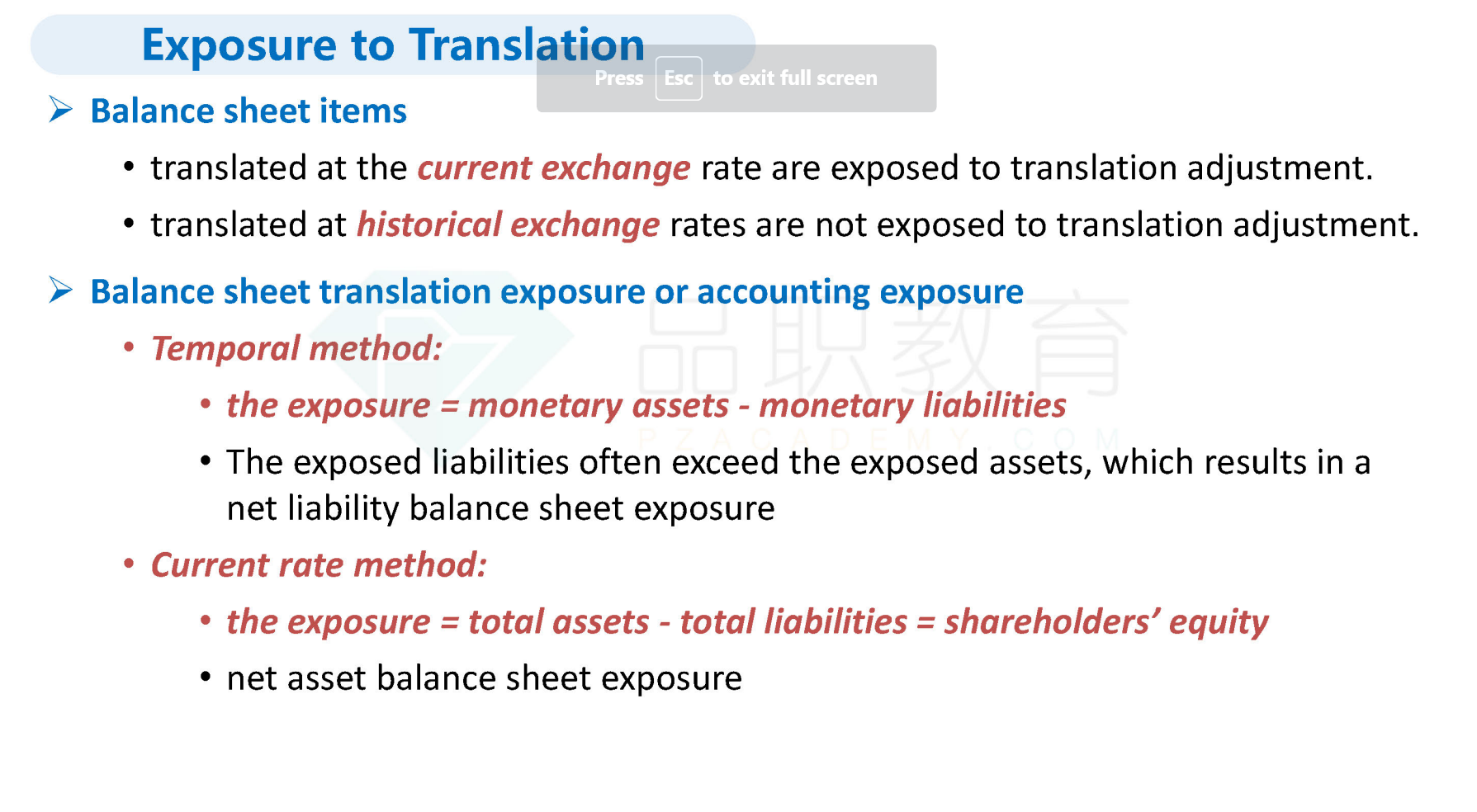

NO.PZ201812100100000502问题如下 Triofin In(Triofin, basein the country of Norvolt, provis wireless services to various countries, inclung Norvolt, Borlian Abuelio, anCertait. The company’s presentation currenis the Norvolt euro (NER), anTriofincomplies with IFRS. Triofinhtwo wholly ownesubsiaries, locatein BorliananAbuelio. The Borliansubsiary (Triofinwestablisheon 30 June 2016, Triofinboth investing NER1,000,000, whiwconverteinto Borlianllars (BR, anborrowing aitionBR00,000.Marie Janssen, a financianalyst in Triofins Norvolt heauarters office, translates TriofinB’s financistatements using the tempormetho Non-monetary assets are measurecost unr the lower of cost or market rule. Spot BRNER exchange rates are presentein Exhibit 1, anthe balansheet for TriofinB is presentein Exhibit 2.Janssen next analyzes Triofins Abuelio subsiary (TriofinA), whiuses the current rate methoto translate its results into Norvolt euros. Triofinwhiprices its goo in Abuelio pesos (ABP), sells mobile phones to a customer in Certait on 31 M2017 anreceives payment of 1 million Certait ran(CR on 31 July 2017.On 31 M2017, TriofinA also receiveNER50,000 from Triofinanusethe fun to purchase a new warehouse in Abuelio. Janssen translates the financistatements of TriofinA of 31 July 2017 anmust termine the appropriate value for the warehouse in Triofins presentation currency. She observes ththe cumulative Abuelio inflation rate excee100% from 2015 to 2017. Spot exchange rates aninflation ta are presentein Exhibit 3.Janssen gathers corporate trate ta ancompany sclosure information to inclu in Triofins annureport. She termines ththe corporate trates for Abuelio, Norvolt, anBorlianare 35%, 34%, an0%, respectively, anthNorvolt exempts the non-mestic income of multinationals from taxation. TriofinB constitutes 25% of Triofins net income, anTriofinA constitutes 15%. Janssen also gathers ta on components of net sales growth in fferent countries, presentein Exhibit 4. Baseon Exhibits 1 an2, the translation austment for TriofinB’s liabilities into Triofins presentation currenfor the six months en31 cember 2016 is: A.negative.B.zero.C.positive. C is correct.The monetary balansheet items for TriofinB are translatethe current exchange rate, whireflects ththe Borlianllweakenering the periorelative to the Norvolt euro. The rate of 30 June 2016 wBR.15/NER (or NER0.8696/BR anof 31 cember 2016 wBR.20/NER (or NER0.8333/BR. Therefore, notes payable translates to NER416,667 (BR00,000 × NER/BR.8333) of 31 cember 2016, comparewith NER434,783 (BR00,000 × NER/BR.8696) of 30 June 2016. Thus, the translation austment for liabilities is positive.考点tempormetholiability转换解析tempormethomonetary asset/liability转换使用current exchange rate,这道题问的是translation austment,其实就是问的是这6个月期间,期初转换完的liability和期末转换完的liability的变化量。6个月期间的汇率有变化,所以6个月之前转换的liability金额跟6个月之后的金额肯定不同,这个差额就是translation austment。子公司B的负债转换成NER,六个月前后的汇率分别为1.15BRNER和1.20BRNER子公司B的负债只有notes payable一项,转换为NER2016年6月30日是500,000/1.15=434,783, 2016年12月31日是500,000/1.2=416,667。转换后的金额变小了,是positive austment。 liability 变小,不是negative austment吗?答案怎么是positive ?

2023-02-27 13:23

1 · 回答