NO.PZ2023021601000029

问题如下:

The following table shows data for the stock of JKU and a market index.

Based

on the capital asset pricing model (CAPM), JKU is most likely: (2016

选项:

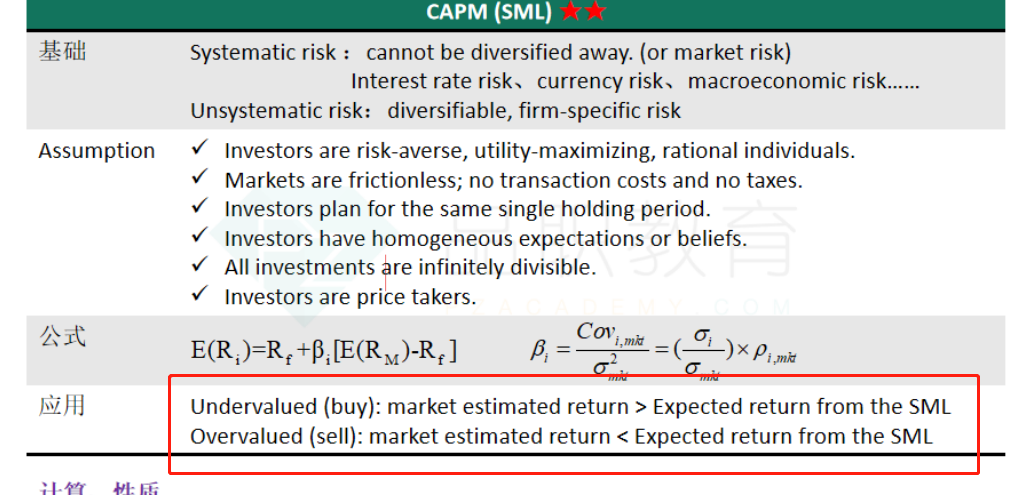

A.overvalued. B.fairly valued. C.undervalued.解释:

βJKU = ρJKU,M × σJKU/sM = 0.75 × 0.2/0.15 = 1.0 and E(RJKU) = RFR + βJKU x (RM – RFR) = 0.05 +1 x (0.12 – 0.05) = 0.12. The required rate of return of JKU is 12%, and the expected return of JKU is 15%. Therefore, JKU is undervalued relative to the security market line (SML); the risk–return relationship lies above the SML.