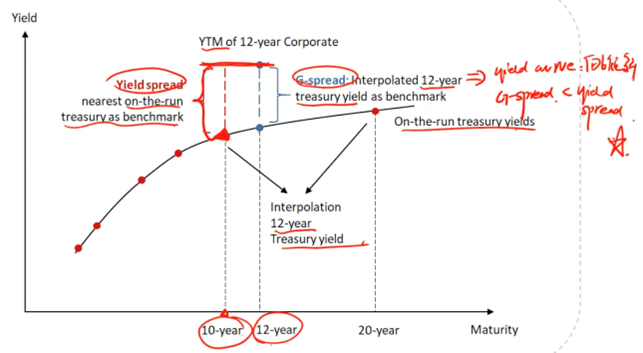

根据这张图,有这么一个结论:Yield spread is higher than G-spread: government bond used has a shorter maturity than the corporate bond, and the government yield curve is upward-sloping.

图上看,G-spread采用12年期债权,yield spread采用近似的10年期债权,government bond has a longer maturity than the corporate bond,为什么结论反而是shorter?