这道题为什么不能选1 cash equivalent不也是可以match cf吗 而且Sharpe Ratio还高

lynn_品职助教 · 2023年07月18日

嗨,从没放弃的小努力你好:

这道题为什么不能选1 cash equivalent不也是可以match cf吗 而且Sharpe Ratio还高

cash不能很好地match。

cash没有抗通胀的能力,因为我们需要cover liability,hedging portfolio的影响因素应当与liability的影响因素相同。

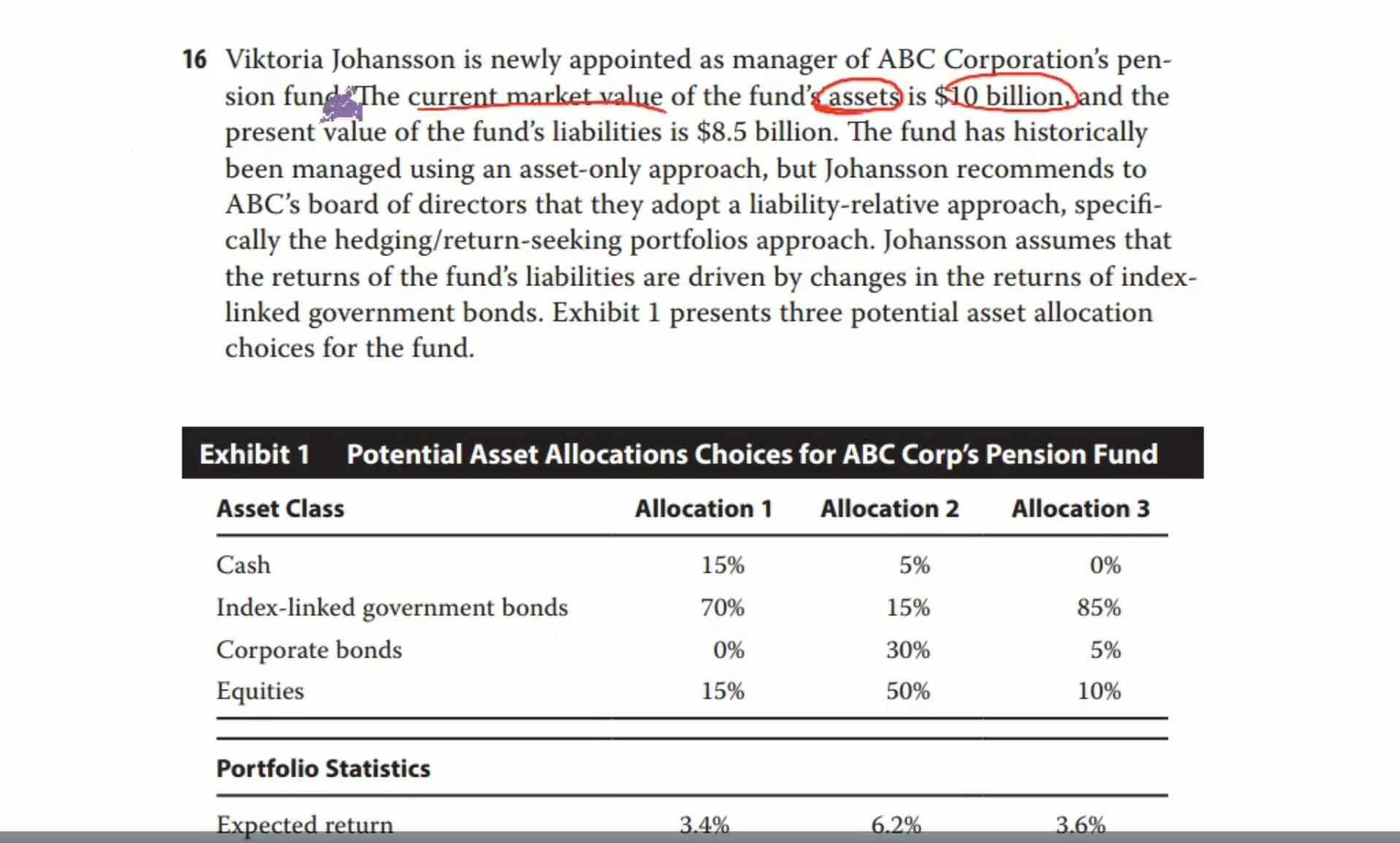

文中说 Johansson assumes that the returns of the fund’s liabilities are driven by changes in the returns of index-linked government bonds. 也就是说能够很好地匹配fund liabilities的是 index-linked government, 而Allocation 3 的 index-linked government占比正好是85%,所以最合适。

cash虽然很稳健但是抗不了通胀,另外,既然是债券,定期是可以拿到coupon的,投资cash没有coupon,不能跟fund liability的现金流相匹配。

Allocation 1的 index-linked government的占比是70%,少于85%(在不考虑cash的情况下),虽然 equity 投的更多,但是不能很好的hedging liabilities。

----------------------------------------------努力的时光都是限量版,加油!