NO.PZ202208220100000302

问题如下:

You are a junior analyst at an asset management firm. Your supervisor asks you toanalyze the return drivers for one of the firm’s portfolios. She asks you to constructthree regression models of the portfolio’s monthly excess returns (RET),starting with the following factors: the market excess return (MRKT), a value factor(HML), and the monthly percentage change in a volatility index (VIX). Nextyou add a size factor (SMB), and finally you add a momentum factor (MOM).Your three models are as follows:

Your supervisor is concerned about conditional heteroskedasticity in Model 3 and asks you to perform the Breusch–Pagan (BP) test. At a 5% confidence level, the BP critical value is 11.07. You run the regression for the BP test; the results are shown in Exhibit 1.

Now the chief investment officer (CIO) joins the meeting and asks you to analyze two regression models (A and B) for the portfolio he manages. He gives you the test results for each of the models, shown in Exhibit 2.

The CIO also asks you to test a factor model for multicollinearity among its four explanatory variables. You calculate the variance inflation factor (VIF) for each of the four factors; the results are shown in Exhibit 3.

Identify the type of error and its impacts on regression Model A indicated by the data in Exhibit 2.

选项:

A.Serial correlation, invalid coefficient estimates, and deflated standard errors.

B.Heteroskedasticity, valid coefficient estimates, and deflated standard errors.

C.Serial correlation, valid coefficient estimates, and inflated standard errors.

解释:

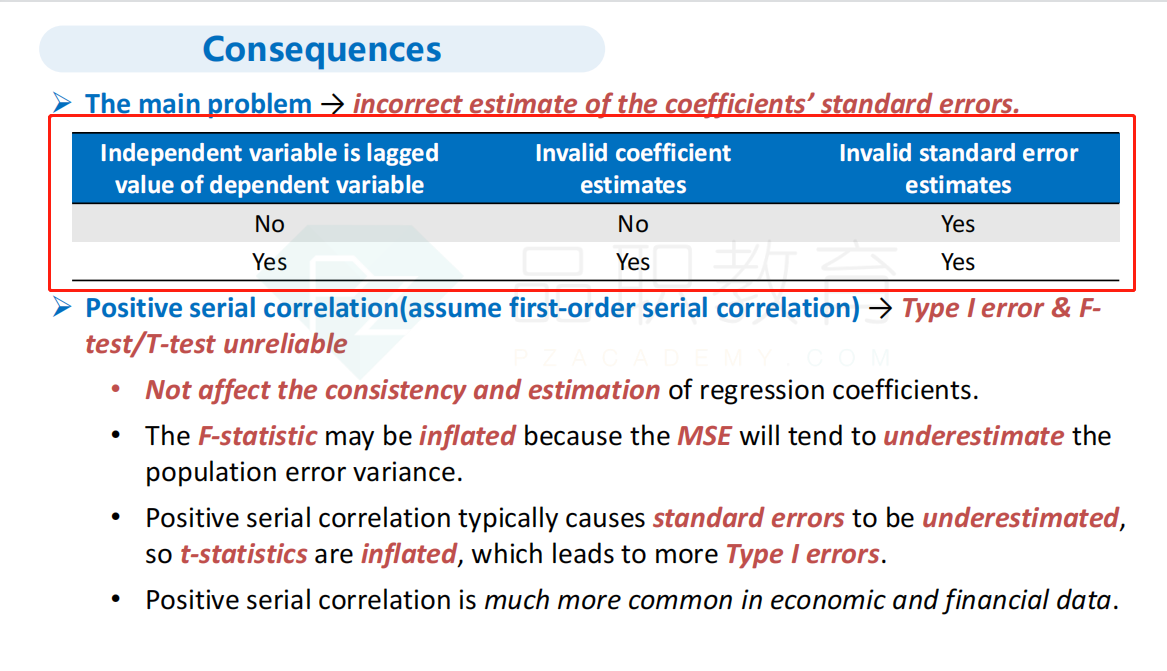

A is correct. The Breusch–Godfrey (BG) test is for serial correlation, and for Model A, the BG test statistic exceeds the critical value. In the presence of serial correlation, if the independent variable is a lagged value of the dependent variable,then regression coefficient estimates are invalid and coefficients’ standard errors are deflated, so t-statistics are inflated.

类比为正向序列相关,系数bo bi不受影响,不受影响是否可以说是有invalid?

这个条件来的。

这个条件来的。