NO.PZ201710200100000408

问题如下:

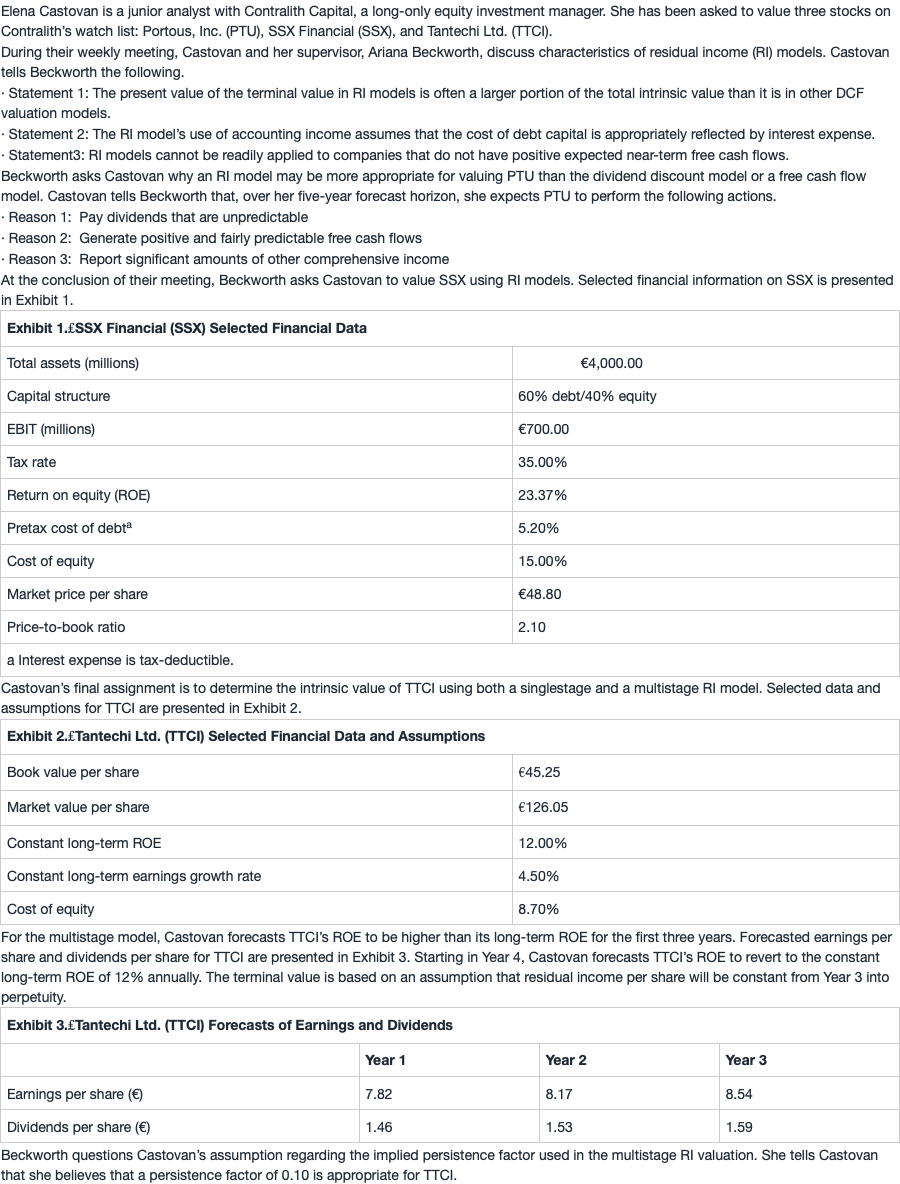

8. Based on Exhibits 2 and 3 and the multistage RI model, Castovan should estimate the intrinsic value of TTCI to be closest to:

选项:

A.€54.88.

B.€83.01.

C.€85.71.

解释:

C is correct.

Residual income per share for the next three years is calculated as follows.

Because Castovan forecasts that residual income per share will be constant into perpetuity, equal to Year 3 residual income per share, the present value of the terminal value is calculated using a persistence factor of 1.

Present value of terminal value =

= =33.78

So, the intrinsic value of TTCI is then calculated as follows.

V0=\frac{45.25+3.88/1.087+3.68/(1.087)^2+33.78}=85.71

1、方法二: RI4=RI3 = 3.47, PVRI' =3.47/0.087 =39.8851

V0 = B0 + RI1/(1+r) + RI2/(1+r)^2 + RI3/(1+r)^3+PVRI'/(1+r)^3 = 45.25 + 3.88/1.087 + 3.68/1.087^2 + 3.47/1.097^3 + 39.8851/1.097^3 =85.71

第三年和以后的分母应该是1.087^3,而不是1.097^3。对吗?

2 如何从题干中判断w=1?

3 是否ROE恒定,RI就恒定?

4 计算RI3,可否用(ROE-RE)*BV2,ROE=12%