NO.PZ2019010402000026

问题如下:

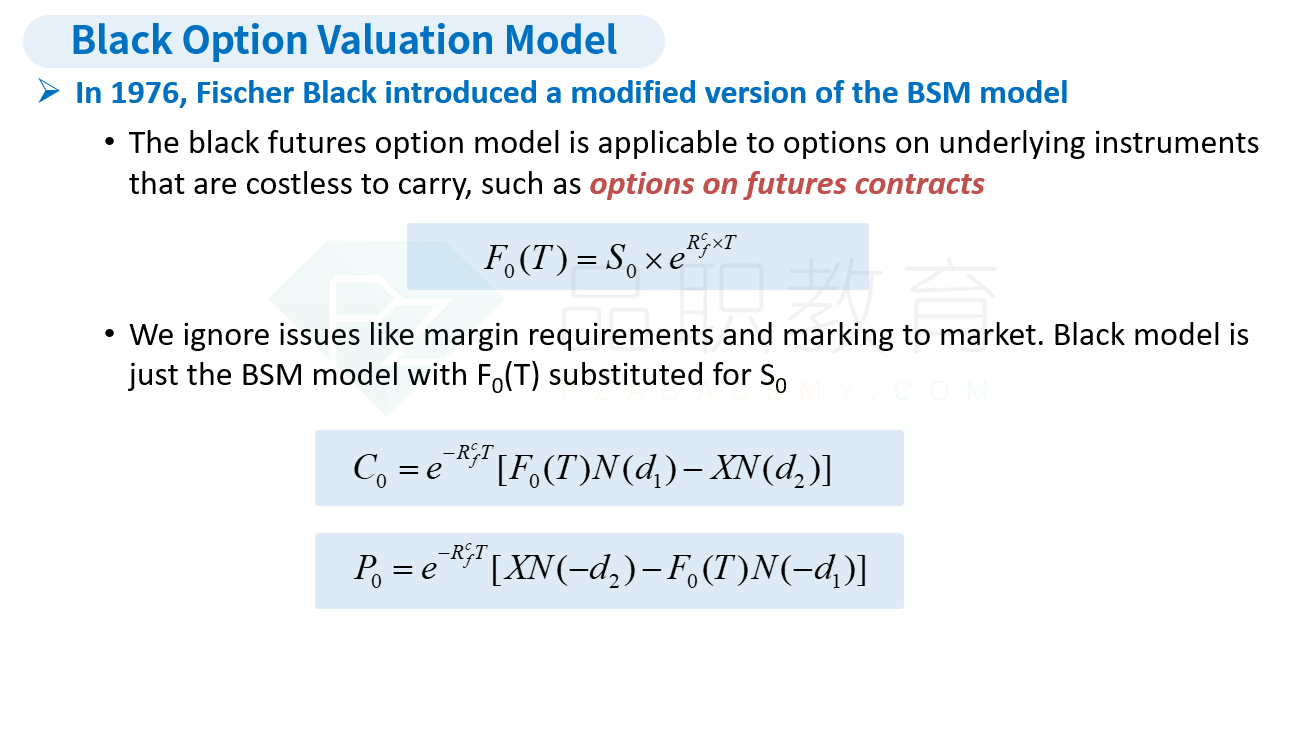

Which of the following would be an input as spot value in the Black model?

选项:

A.S&P 500 index price

B.the price of a futures contract on the S&P 500 index

C.both

解释:

B is correct.

考点:Black model

解析:

Black model可以用来对基础资产为futures/forward、int rate或者swap的option定价,当基础资产为futures时,spot value应该是futures的价格。

可否贴一些对应讲义或者知识点啊?