NO.PZ2018122701000049

问题如下:

A portfolio consists of options on Microsoft and AT&T. The options on Microsoft have a delta of 1000, and the options on AT&T have a delta of 20000. The Microsoft share price is $120, and the AT&T share price is $30. Assuming that the daily volatility of Microsoft is 2% and the daily volatility of AT&T is 1% and the correlation between the daily changes is 0.3, the 5-day 95% VaR is

选项:

A.26193

B.25193

C.27193

D.24193

解释:

A is correct.

考点:Mapping to Option Position

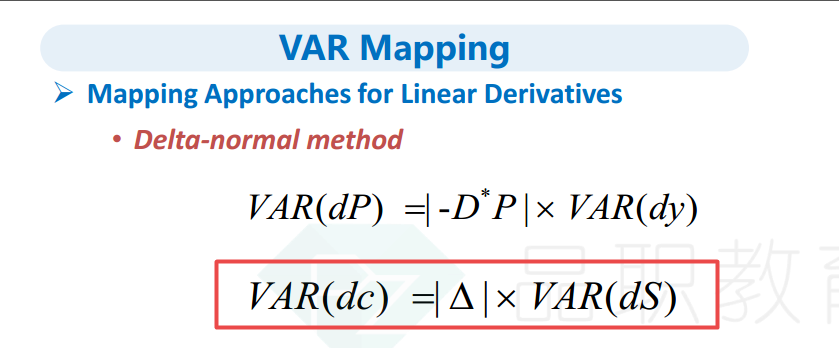

解析:VaRMic= 1.65 × 2% × 120 × 1000 = 3960

VaRAT&T= 1.65 × 1% × 30 × 20000=9900

和讲义上的公式不一样,能否请老师讲答案公式每一项对应的数值含义说明一下,谢谢